If you are researching your next career move at 11:00 PM after a long shift or while the kids are finally asleep, you probably have one burning question:

Can you get a California real estate license Read more...

If you are researching your next career move at 11:00 PM after a long shift or while the kids are finally asleep, you probably have one burning question:

Can you get a California real estate license online?

The short answer is: Mostly, but not entirely.

While the California Department of Real Estate (DRE) has embraced digital transformation—allowing you to complete your education and submit your paperwork from your couch—there are still physical "gatekeepers" that require you to show up in person.

The Reality Check: Online vs. In-Person

What You CAN Do Online

What You MUST Do In Person

Complete all 135 hours of pre-licensing courses.

Sit for the actual State Exam at a DRE exam center.

Submit your application via eLicensing.

Get your Live Scan (digital) fingerprints taken.

Pay your application and license fees.

Present valid government-issued photo ID.

Manage your license renewals later on.

Physically attend the testing center.

The Bottom Line: You can complete 100% of your required education online, but the State of California requires you to physically appear for your exam and your background check. It is important to check the fine print: while the "schooling" is digital, the "licensing" still has a few real-world milestones.

Defining "Online" in the California Licensing Process

When people ask about getting a California real estate license online, they are usually referring to the flexibility of the curriculum. In California, you are required to complete three college-level courses: Real Estate Principles, Real Estate Practice, and one elective.

At ADHI Schools, we’ve spent over 20 years helping students navigate this. We know that for a busy professional, the ability to take online real estate courses in California is the difference between starting a career and just dreaming about one.

However, the "license" itself isn't a digital download. It is a credential granted by the state after you prove your knowledge in a proctored, high-security environment.

The 18-Day Regulatory Rule For Coursework

In California, DRE regulations specify that a student must spend a minimum amount of time with their course materials before they are eligible to take a final exam. This is typically implemented as a seat-time requirement of 18 days per course. Because you must take three courses, your total minimum education time is 54 days—a timeline that applies even if you are the fastest reader in the state.

Step-by-Step: What Parts Can Be Done Online?

To help you plan, here is the numbered flow of the licensing process, showing exactly where the "online" part ends and the "real world" begins.

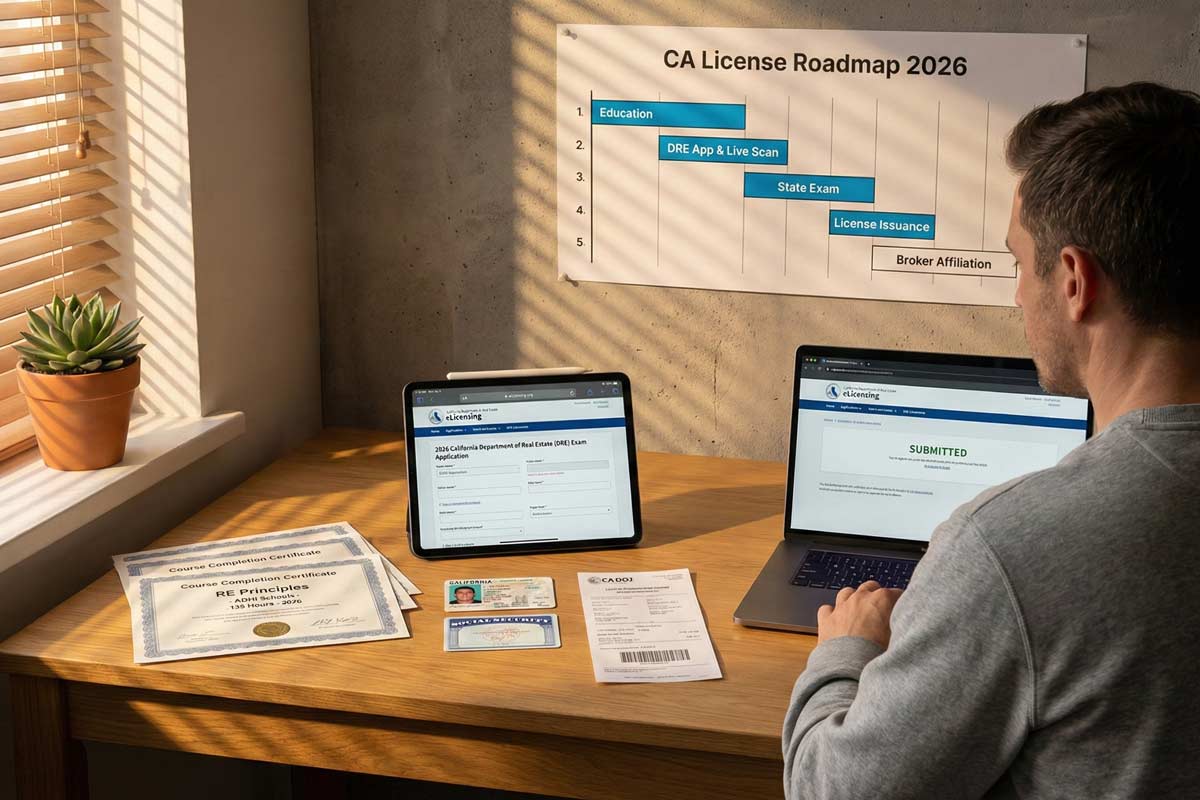

Pre-Licensing Education (Online): Complete your three courses (Real Estate Principles, Practice, and an elective). This takes a minimum of 54 days due to mandated study timers.

Application Submission (Online): Use the DRE eLicensing system to submit your combined Exam/License application.

Live Scan Fingerprints (In Person): You must visit a Live Scan provider to have your fingerprints electronically transmitted to the DOJ and FBI.

The State Exam (In Person): Once your application is processed, you will schedule a date to visit one of the five DRE testing centers (Sacramento, Oakland, Fresno, La Palma, or San Diego).

License Issuance (Digital/Mail): Once you pass, the DRE processes your results. You can often see your license number online before the paper certificate even arrives.

What Must Be Done In Person (And Why)

The DRE takes the integrity of the real estate profession seriously. The reasons you can't do it all from a laptop come down to two things:

Security and Compliance.

Exam Integrity: To prevent cheating and ensure that the person taking the test is actually the applicant, exams are held in monitored facilities where phones and notes are prohibited.

Identity Verification: Live Scan fingerprinting ensures that your criminal background check is tied to your actual identity, which requires a physical "chain of custody" at a licensed provider.

Expert Tip: If you’re in a rush, you’ll want to look into the fastest way to get a real estate license in California.

Timeline Planning

If you are trying to map out your calendar, your "online" progress is the most predictable part of the journey. Once you move into the "in-person" phase, you are at the mercy of DRE processing times and exam seat availability.

For most students, a realistic schedule involves finishing the online coursework while simultaneously preparing their paperwork. For a detailed breakdown of these phases, check out our California real estate license timeline. If you're wondering how those months look on a week-to-week basis, read our deep dive on how long it takes to become a real estate agent in CA.

Cost & Convenience Reality Check

While you save time and gas money by choosing to get a real estate license online in California, you still need to budget for the state-mandated fees.

As of 2026, the DRE fee for a salesperson exam is $100, and the original license fee is $350, totaling $450 paid directly to the state. Additionally, you will need to account for Live Scan fingerprinting. This involves a $49 state processing fee, plus a "rolling fee" charged by the private provider (typically $30–$45).

For a full breakdown of every nickel and dime, see our guide on how much it costs to get a real estate license in California.

Common Misconceptions

"I can take the state exam from home."

No. You must travel to a DRE-approved testing site.

"Online courses are instant."

No. California law requires you to spend a minimum amount of time with the material (typically 18 days per course).

"Once I finish courses, my license is automatic."

No. Finishing courses only makes you eligible to apply for the state exam.

"Online = instant approval."

Even if you submit online, the DRE may take several weeks to review your file and authorize you to test.

FAQ Section

Can I take the California real estate exam online from home?

No. The California State Exam must be taken in person at one of the Department of Real Estate’s designated testing centers to ensure exam security.

Can I complete the required real estate courses online?

Yes. You can complete all 135 hours of required pre-licensing education (Principles, Practice, and an elective) through an approved online provider like ADHI Schools.

Do I have to do Live Scan in person?

Yes. Live Scan requires a physical scan of your fingerprints by a certified technician at a licensed provider. This cannot be done via a smartphone or home scanner.

How long does it take if I do everything possible online?

Most students finish in 3 to 5 months. This accounts for the 54-day mandatory study period and current DRE administrative processing times.

What is the fastest way to get licensed in California?

The fastest route is to submit a "Combined" Exam and License application and complete your Live Scan immediately after finishing your online courses to avoid "dead time" while waiting for your test date.

How much does it cost to get licensed in California?

You should budget roughly $600 to $1,100 total. This includes your online course tuition, the $450 in DRE exam and license fees, and your Live Scan fingerprinting costs.

What is the most common reason people get delayed?

The most common delay is waiting to schedule the state exam. If you wait until after your courses are finished to start your DRE application, you may find yourself in a weeks-long queue for a testing seat.

Ready to Start Your Journey?

The road to a new career starts with the right map. While you can't do everything online, choosing a flexible, high-quality online education provider is the best way to maintain your current lifestyle while building a new one.

For a comprehensive look at the entire process, visit our California Real Estate License Guide.

|

Seeing the word "PASS" after you leave the Department of Real Estate (DRE) testing center is a massive milestone. You’ve successfully navigated the 150-question hurdle that stalls thousands of aspiring Read more...

Seeing the word "PASS" after you leave the Department of Real Estate (DRE) testing center is a massive milestone. You’ve successfully navigated the 150-question hurdle that stalls thousands of aspiring agents every year.

However, after over 20 years of preparing candidates for this moment, the most important truth I can share is this:

Passing the real estate exam is the end of your studies, but it is only the beginning of the licensing process. Understanding exactly what happens after you pass the CA real estate exam is critical to ensuring you don’t get stuck in a months-long "administrative gap" caused by paperwork errors or timing mistakes.

The Big Distinction: "Pass" vs. "License Issued"

A common mistake new candidates make is assuming they can hit the ground running the second they walk out of the testing center.

The Professional Reality: You do not have a license yet; you have a passing score. You cannot legally perform any activities that require a license—including representing yourself as a licensed salesperson to the public—until the DRE officially issues your license number and your status reflects as "Licensed" in their public database and your license is placed with a broker.

Consider this scenario: A candidate passes on Tuesday, celebrates on social media by calling themselves a "licensed agent," and begins soliciting clients on Wednesday. Because their license hasn't been officially issued, they are technically practicing without a license, which can lead to disciplinary action before their career even begins.

Two Common Paths After You Pass

Your next steps depend entirely on which application path you chose at the beginning of this journey.

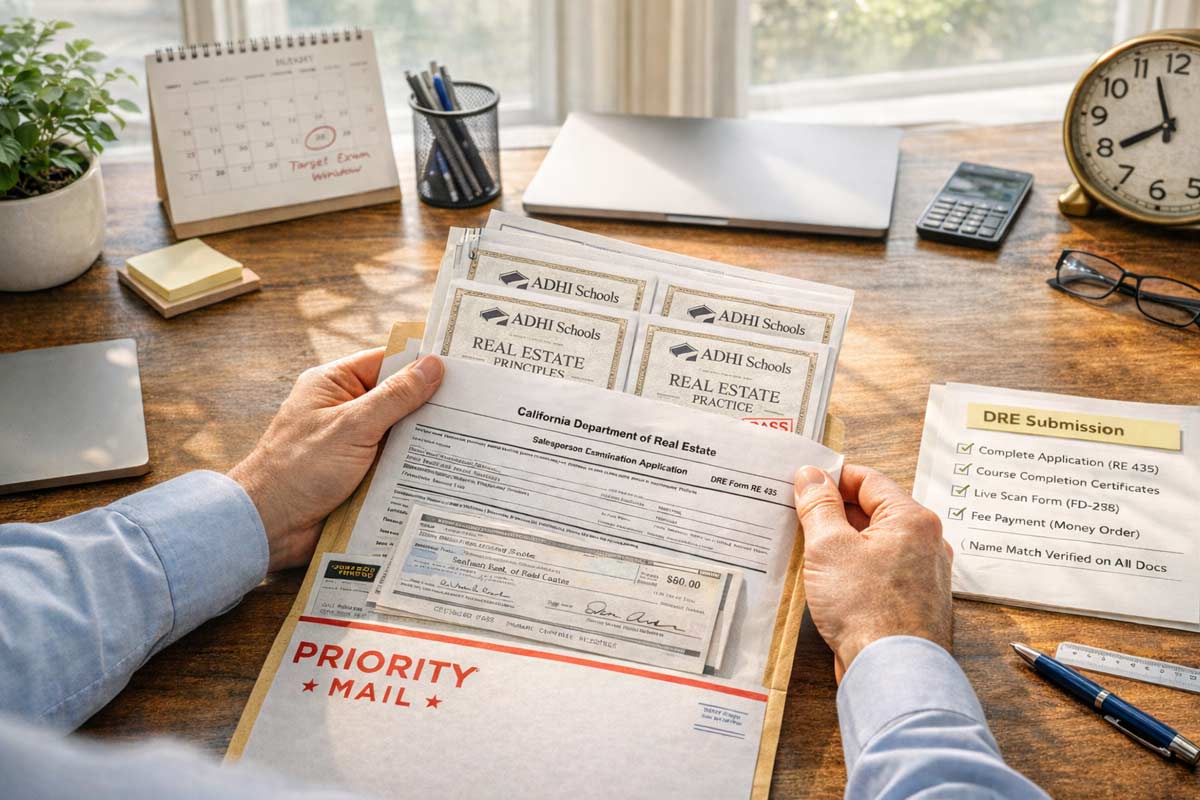

Path 1: Exam + License Combo Applicants

If you filed the Salesperson Exam/License Application (RE 435) and paid both fees upfront, your path is generally the most streamlined.

What Happens Now: The DRE already has your intent to be licensed. Once your passing score is uploaded (usually within a few business days), they move straight to your background check and licensee issuance.

Your Move: Check if your license was issued here. This path is often the fastest when your file is clean and your fingerprints clear quickly.

Path 2: Exam-Only Applicants

If you only applied to take the test using form RE 400A, the DRE has no record of your license application yet.

What Happens Now: You must log into the DRE eLicensing system to download the Salesperson License Application (RE 202). You have exactly one year from your pass date to submit this application; if you miss that window, you must retake the exam - This is one of many reasons ADHI Schools recommends the combo exam/license application.

Your Move: This form must be submitted along with your Live Scan Service Request (RE 237) and the required licensing fee. Follow the DRE instructions for the current submission method (mail or other accepted electronic methods).

Decision Helper: Which path did I choose?

If you paid $450 in DRE fees up front, you are likely a "Combo" applicant. If you only paid the $100 exam fee and never submitted license materials, you are "Exam-Only." You can verify your application history by logging into your DRE eLicensing profile.

The Post-Pass Checklist: Actionable Steps to Your License

To avoid the "delay cycle," follow this checklist with the precision of a professional agent.

Verify Your Identity Consistency: Ensure the name on your application matches your government-issued ID exactly. For a refresher on why name matching is vital for identity consistency, see our guide on Identification Requirements for the CA Exam.

Access Forms via eLicensing: Use the DRE’s eLicensing portal to download your RE 202 (if applicable) and to track your status. Ensure you follow all current DRE instructions for how to submit these documents once completed.

Handle the Live Scan: If you haven't completed your fingerprints, do so immediately. The DRE cannot issue a license until they receive fingerprint responses from the DOJ and FBI.

Secure Your Sponsoring Broker: While the DRE can issue your license as Licensed NBA (No Broker Affiliation), you cannot perform licensed acts or earn commissions until you are affiliated with a responsible broker.

Maintain Professional Standards: Exam-day policies are strict, and the licensing process is strict too—don’t treat either casually. Refer to the California Real Estate Exam Rules & Testing Policies to remember the level of discipline the DRE expects from its applicants.

How Long Does It Take After Passing?

Processing times for after passing the California real estate exam fluctuate based on the DRE’s current volume. The DRE regularly updates their processing timeframes on their website, showing the "as of" dates for the applications they are currently reviewing.

Reviewable files (no missing signatures, correct fees, clear fingerprints) move through the system as soon as they are reached in the queue.

Deficient files (missing initials, mismatched names, or incorrect fees) are sent back to the applicant, which can add significant delays to the timeline.

To speed up the process:

Use the exact, current fee amount

Keep a copy of your Live Scan RE 237 with your ATI number to prove the fingerprints were transmitted.

Ensure all required signatures—including your sponsoring broker’s—are in the correct boxes.

If Something Goes Wrong: The Two Failure Modes

Even after passing, two common issues can stall your career:

The Administrative Loop: This is usually caused by sloppy paperwork. Revisit our list of What to Bring to the California Real Estate Exam as a reminder that professional success always starts with meticulous documentation and clean logistics.

The Support Gap: If you have colleagues who didn't make it this time, they may need to review our guide on What Happens If You Fail the CA Real Estate Exam to help them plan their retake.

Pro-Level Guidance: Think Like a Professional Already

The transition from "student" to "licensee" is your first official real estate transaction. Success in this business depends on paperwork discipline and responsiveness.

Be Meticulous: Real estate is a game of contracts. Treat your RE 202 with the same care you would a million-dollar purchase agreement.

Be Proactive: Check eLicensing regularly to see if your license number has been generated.

Build Habits Early: Use this waiting period to interview brokers and set up your business foundation.

FAQ: Post-Exam Essentials

How long after passing the CA real estate exam do I get my license?

It varies based on the DRE's current queue. "Combo" applicants often see results faster, but separate applications generally take several weeks for processing and background clearance.

Can I work as an agent after I pass the exam?

No. You cannot legally perform any acts requiring a license until your status is officially "Licensed" in the DRE database and you are working under a broker.

What if my name doesn’t match my documents?

This will cause an administrative delay. The DRE requires your legal name to be consistent across your ID, exam record, and background check.

What’s the difference between passing and getting a license issued?

Passing means you've met the testing requirement. "Issued" means the DRE has verified your application, fees, and background, granting you the legal authority to practice.

Your Next Step

Your journey to a successful real estate career is just beginning. To ensure you stay on the right track and avoid common pitfalls, bookmark our master guide:

California Real Estate Exam Guide

|

If you just saw the word "FAIL" on your exam results, take a breath.

The California real estate exam is a rigorous barrier to entry designed to ensure only prepared professionals enter the industry. Read more...

If you just saw the word "FAIL" on your exam results, take a breath.

The California real estate exam is a rigorous barrier to entry designed to ensure only prepared professionals enter the industry. At ADHI Schools, I have spent over 20 years helping thousands of students navigate this exact moment.

What happens if you fail the CA real estate exam isn’t the end of your career—it is a reconnaissance mission. You now have firsthand experience with the testing environment and the specific phrasing of the questions. Here is your professional recovery plan to turn this detour into a license.

First: What Failing Actually Means

Procedurally, failing simply means you didn’t hit the required scoring threshold. According to the California Department of Real Estate (DRE) standards:

Salesperson Candidates: Must score at least 70%.

Broker Candidates: Must score at least 75%.

Quick Snapshot: Your Immediate To-Do List

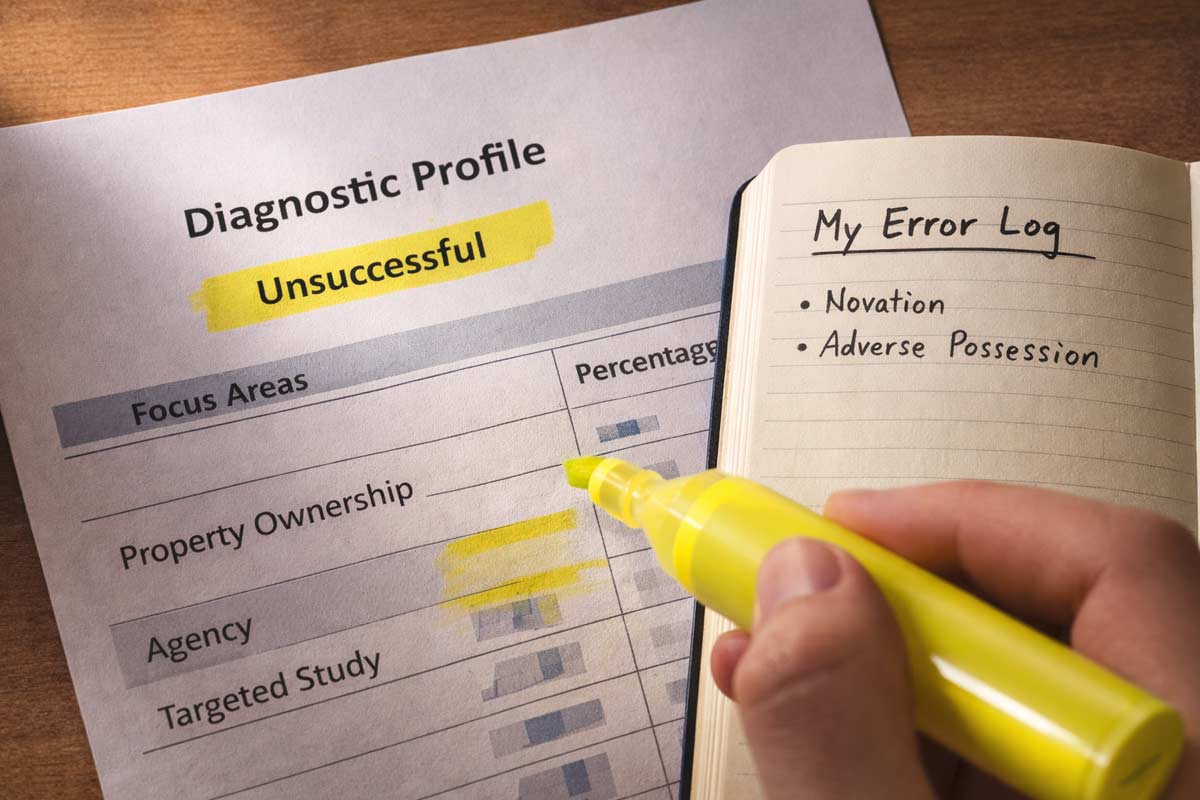

Review Today: Analyze your diagnostic profile to see which of the seven categories (e.g., Property Ownership, Land Use) need work.

Confirm Eligibility: Ensure you are still within your two-year application window.

Wait for the System: Do not attempt to reschedule until the DRE has fully processed your "Unsuccessful" result.

What Happens Immediately After You Fail

In California, you typically receive your results at the testing center. If you didn’t pass, you will receive a notification containing a diagnostic profile. This document is your roadmap; it breaks down your performance percentage in each major category.

The "Golden Hour" Reconnaissance

Before the specific details of the questions fade, perform a "brain dump":

Recall 10 Questions: Write down ten topics or specific questions that confused you.

Analyze Pacing: Did you finish with an hour to spare, or were you rushing to beat the clock?

The "Strategy" Check: Did you change your answers frequently? Real-world scenario: We often see students second-guess themselves from a passing score down to a failing one. Trust your first instinct.

Protecting Your Focus

Avoid a "panic spiral" by staying off unverified forums or Reddit. Every test-taker’s experience is subjective; trust your official diagnostic data over internet anecdotes that may lead to conflicting advice or wasted study time.

How to Retake the Exam

To reschedule the CA real estate exam, you must apply for a re-examination and pay the current fee.

The Re-Examination Rules

The Two-Year Eligibility Window: You must pass the examination within the two-year period following the date your initial application was filed. If you do not pass within this window, your application expires, and you must re-establish eligibility to try again.

Waiting for Results: DRE does not publish a fixed "waiting period" (such as 30 days) between attempts. However, you must wait until your results have been officially processed and received before you are eligible to reapply.

The "Submit Once" Rule: DRE explicitly warns candidates to submit their reschedule application only once—either online or by mail. Multiple submissions can lead to duplicate charges or your records being flagged for review.

One Date at a Time: You can only be scheduled for one exam date at a time. Rescheduling an existing appointment typically removes your current date.

Avoid the "System Flag": Attempting to obtain a new exam date before your previous results are processed can result in your records being withheld and the assessment of additional fees.

Verify Your Logistics

Before you head back, review the Identification Requirements for the CA Exam and the California Real Estate Exam Rules & Testing Policies to ensure no administrative errors disrupt your next attempt.

Why People Fail (and How to Fix It Fast)

Most failures fall into one of four patterns. Identify yours to adjust your strategy:

Failure Pattern

What it looks like

The Professional Fix

The Content Gap

Seeing terms like "Novation" or "Adverse Possession" and feeling lost.

Focus on the glossary. Real estate is a vocabulary test at its core.

The Strategy Gap

Narrowing it to two answers and always picking the wrong one.

Practice the "distractor" method: find why three answers are wrong instead of why one is right.

The Physiology Gap

Crashing or losing focus around question 100.

Build stamina. Take full-length, timed sets to mimic the 3-to-4-hour window.

The Logistics Gap

Arriving stressed due to traffic, ID issues, or prohibited items.

Review What to Bring to the California Real Estate Exam 48 hours early.

The 14-Day Comeback Plan

Don’t wait months to retake. Momentum is your ally.

Days 1–3 (Weakness Blitz): Study the two lowest-scoring categories on your diagnostic profile.

Days 4–7 (The Error Log): Take practice questions and write down why you missed them. Understanding the "why" prevents repeat mistakes.

Days 8–11 (Simulated Testing): Take full-length sets (150 questions for Salesperson, 200 for Broker). Build your sitting stamina for the actual 3-to-4-hour exam window.

Days 12–13 (High-Probability Review): Review Agency, Contracts, and Practice of Real Estate and Mandated Disclosures.

Day 14 (The Reset): Light review only. Confirm your location and pack your ID.

Simulating Success: The CrashCourseOnline.com Method

If your diagnostic profile showed gaps in specific areas, the most common mistake is to "just study more." You don't need more study; you need simulation. While nobody has the exact questions that are on the test, our proprietary system at crashcourseonline.com is engineered to closely simulate the concepts tested on the exam. We categorize our 1,100+ practice questions into the same seven categories found on your official results notice, allowing you to hyper-focus on your weakest subjects.

Frequently Asked Questions

How soon can I retake the California real estate exam?

DRE does not publish a fixed numeric wait time; however, you must wait until your current results are processed and received before the system will allow you to reapply.

How do I reschedule or reapply after failing?

The most efficient method is using the DRE eLicensing portal. You will select "Re-Examination," pay the fee, and select a new date.

Do my pre-license course certificates expire?

No. According to the DRE, pre-license course approvals for the three required college-level courses do not expire. You only need to focus on passing the state exam itself.

What happens if my two-year application window expires?

If you don't pass within two years of your application date, you must submit a new application, pay the initial fees, and re-establish eligibility.

Your Next Steps

This attempt didn't give you a license, but it gave you data. Now, we execute the plan. Once you clear this hurdle—and you will—you can look forward to What Happens After You Pass the CA Real Estate Exam.

For a comprehensive look at the entire journey, consult our California Real Estate Exam Guide.

Step 1: Download your diagnostic profile from the DRE eLicensing portal.

Step 2: Schedule your re-exam once the system allows to lock in your momentum.

Step 3: Start your Error Log based on your 10 "reconnaissance" questions.

Need a hand with the data?

If you have your diagnostic profile and aren't sure how to prioritize your study hours, reach out. We can help you build a targeted schedule based on your specific score breakdown.

|

You’ve spent weeks, perhaps months, mastering contracts, disclosures, and agency relationships. But the most stressful part of the California real estate exam should be making sure you pass the first Read more...

You’ve spent weeks, perhaps months, mastering contracts, disclosures, and agency relationships. But the most stressful part of the California real estate exam should be making sure you pass the first time, not getting through the front door of the testing center.

Every year, well-prepared candidates are turned away before they even see a single exam question.

Why?

Because they forgot a specific document, brought a prohibited item, or arrived with an ID that didn't match their registration. At ADHI Schools, I have spent over 20 years guiding students through this process, and we’ve seen how a simple oversight can derail a career launch.

This is your definitive "bring / don't-bring" checklist. Use this guide to ensure your exam day is focused on the content, not the logistics.

Quick Checklist Preview

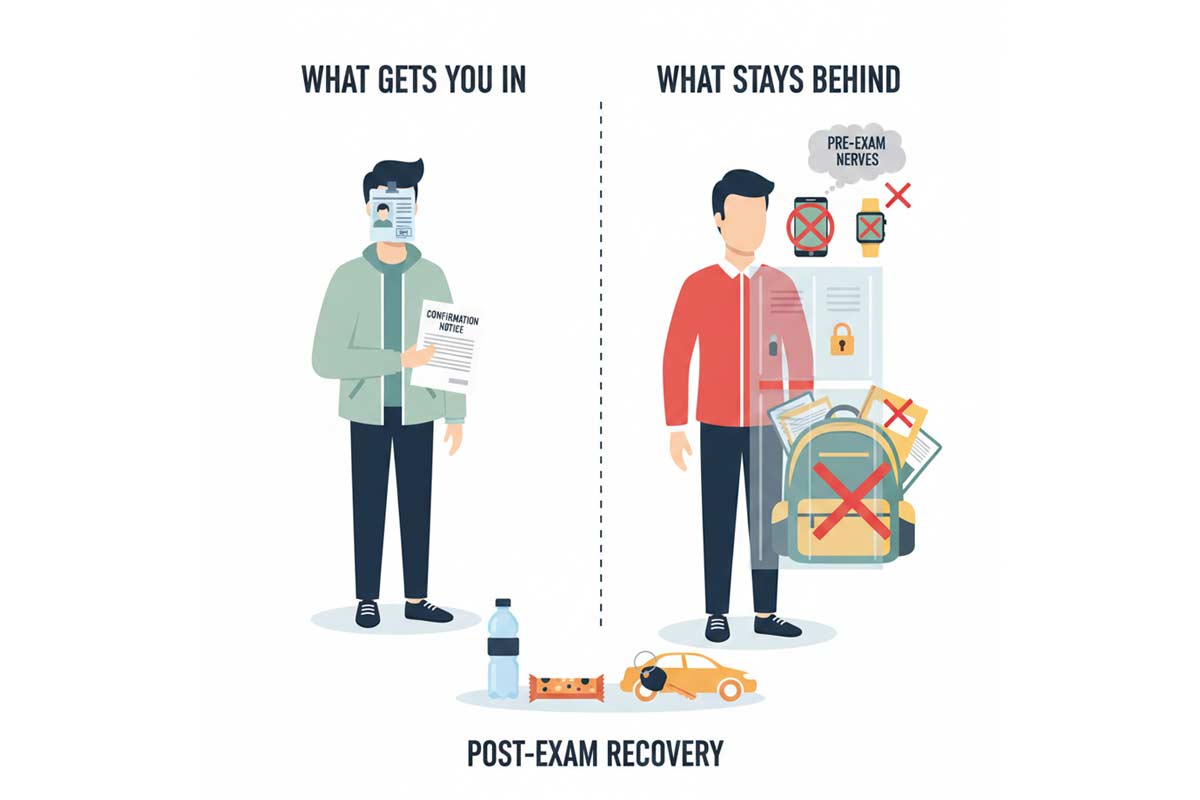

Must Bring: Valid Government-issued Photo ID and Exam Confirmation.

Must Leave: All electronics (phones, smartwatches) and study materials.

Arrive: At least 30 minutes early to handle security and storage.

Can I bring my phone to the California real estate exam?

No. Store it in your locker or leave it secured in your vehicle. Even powered-off devices can trigger a rule violation if they are on your person during the exam.

The 60-Second Checklist (Bring / Don’t Bring)

If you are walking out the door right now, here is the high-confidence version of your day.

BRING THESE

LEAVE THESE (Car or Home)

Valid, current Photo ID

Your Smartphone / Tablet

Printed Exam Confirmation Notice

Smartwatches or Fitbits

A sweater or light jacket

Notebooks, textbooks, or "cheat sheets"

Your car keys (to be stored in a locker)

Bulky backpacks

A calm, focused mindset

Large bags or

Mandatory Items You Must Bring

To sit for the exam, you must prove who you are and that you are authorized to be there. The proctors at the testing center have zero flexibility on these requirements.

1. Valid Government-Issued Photo ID

This is the most common point of failure. Your ID must be current (not expired), contain a recognizable photograph, and—most importantly—the name on your ID must match the name on your exam registration.

For a deep dive on what counts as valid (and what causes a turn-away), see Identification Requirements for the CA Exam.

2. Your Exam Confirmation Notice

While many centers can look you up digitally, having a printed copy of your examination confirmation (obtained via the DRE eLicensing system) is your "golden ticket." It contains your exam date, time, and center location. It serves as your proof of scheduling if there is a technical glitch at the check-in desk.

Optional Items That Help (Without Getting You in Trouble)

While the list of what you can take into the testing room is tiny, these items will make your overall experience significantly better:

Layered Clothing: Testing centers are notorious for unpredictable climates. One room might be a freezer, the next a sauna. Bring a light jacket or sweater (without many pockets) so you can adjust.

Parking Plan and Buffer Time: Don't let a hunt for a parking spot raise your cortisol levels. Map out the center 24 hours in advance and aim to be in the parking lot 45 minutes before your start time.

Water and a Snack: You cannot bring these into the testing room, but keep them in your car. After hours of intense mental focus, your blood sugar will be low. Having a "recovery snack" waiting for you is a pro move.

What Not to Bring (Common Turn-Away Triggers)

The California Department of Real Estate (DRE) and its testing partners maintain strict security protocols. Bringing these items into the testing area is often considered a security violation.

Electronics of Any Kind: This includes phones, tablets, and e-readers.

If you leave your phone in your pocket and it's discovered during check-in—even if it's powered off—it can be flagged as a violation.

Watches and Wearable Tech: Smartwatches are strictly prohibited. Policies on analog watches vary by site; to avoid any confusion or delays, it is best to leave all watches in your locker or car.

Calculators: Calculators are no longer provided at the exam site and you aren’t allowed to bring your own. There is no longer any math on the real estate exam.

Bags and Wallets: Most centers provide small lockers, but they are often only large enough for a set of keys and a slim wallet. Avoid bringing large purses or backpacks.

To avoid accidental rule violations, review California Real Estate Exam Rules & Testing Policies before exam day.

What to Expect at Check-In (So Nothing Surprises You)

Checking in for the exam feels a bit like TSA at the airport. You should arrive at least 30 minutes early to ensure you aren't rushed.

The Security Sweep: You may be asked to empty your pockets, turn them inside out, and show your wrists to ensure no prohibited items are being brought in.

The Storage Reality: You will likely be assigned a small locker for your keys and ID. Note that the DRE and the test center take no responsibility for lost or stolen items—leave everything but the essentials in your locked vehicle.

The Name Match: The proctor will compare your ID to the roster. If the names don't match and you lack the documentation mentioned above, you may not be allowed to test.

If You Get Turned Away (Your Next Move)

If the worst happens—you're late, your ID is expired, or you forgot your documents—take a breath. It feels like a disaster, but it is a fixable mistake.

If you are turned away, you will typically have to reschedule and pay a new examination fee. Once you've processed the frustration, you'll need a recovery plan. If you are unable to complete the exam for any reason, check out our guide on What Happens If You Fail the CA Real Estate Exam to learn how to reapply and get back on track.

After the Exam: What Comes Next

When you finish the exam, the screen will eventually reveal your result. Passing is an incredible milestone, but it’s just the start of the licensing process. If you haven’t done your fingerprints yet you will need to do that and apply for your license.

ADHI Schools recommends the combo exam/license application that allows for the exam and license to be applied simultaneously.

For a step-by-step look at how to turn that passing score into an active license, read our breakdown: What Happens After You Pass the CA Real Estate Exam.

FAQ: California Real Estate Exam Day

What ID do I need to bring to the California real estate exam?

You need a current, government-issued photo ID such as a Driver’s License, State ID card, or Passport.

Do I need to print my exam confirmation to take the test?

While not always strictly required at every center, it is highly recommended. It serves as your "receipt" and contains vital information if there is a scheduling dispute.

Can I bring my phone into the exam room?

Absolutely not. Phones must be powered off and stored in a locker or left in your vehicle.

Are smartwatches allowed during the California real estate exam?

No. Smartwatches are treated as prohibited communication devices.

What happens if I arrive late to the exam center?

Most centers enforce a strict cutoff window. If you arrive late, you may be treated as a no-show and required to reschedule—your exam confirmation notice controls the timing rules.

Is there a locker for personal belongings at the test center?

Most testing locations provide small lockers for essential items like keys and wallets, but they cannot accommodate large bags or laptops.

Your Full Exam Roadmap

Looking for the "Big Picture"? Our California Real Estate Exam Guide is the master hub for scheduling, rules, ID, and what to do after you pass or fail.

Printable Checklist

Primary ID: Current, valid, and matches registration name.

Confirmation Notice: Printed from eLicensing.

The "Light" Setup: No heavy bags, no extra tech.

Vehicle Prep: Phone and watch hidden/locked in the car.

Timeline: Directions saved, arriving 30–45 mins early.

Need a focused prep plan? Explore our www.crashcourseonline.com to get exam-ready once you’ve mastered the logistics.

Or warm up with our Free Real Estate Practice Exam to get familiar with question style before test day.

|

Last Reviewed: February 2026 (Always verify the latest rules on the official California Department of Real Estate (DRE) website before your exam day.)

Quick Summary (TL;DR): To sit for the California Read more...

Last Reviewed: February 2026 (Always verify the latest rules on the official California Department of Real Estate (DRE) website before your exam day.)

Quick Summary (TL;DR): To sit for the California real estate exam, you must present a valid government-issued photo ID that matches your registration name. Electronic devices—including phones and smartwatches—are prohibited in the testing room. Plan to arrive at least 30 minutes early; severely late arrivals are often denied entry and may need to reschedule.

The biggest obstacle to passing your California real estate exam shouldn’t be the check-in desk. Every year, qualified candidates are turned away or disqualified—not for lack of study, but for violating a small set of non-negotiable exam-day rules.

With over 20 years of preparing candidates, I have seen the preventable errors that delay months of hard work. This guide cuts through the anxiety and gives you the rules you need so your only job on exam day is answering questions.

The 80/20 Rule: The Policies That Most Often Get Candidates in Trouble

Most exam-day issues stem from a handful of avoidable mistakes. Focus your attention here:

Identification issues: An invalid, expired, or unacceptable ID is the fastest way to be denied entry.

Prohibited personal items: Phones, watches, bags, and even your own pens can trigger disqualification if brought into the testing room.

Late arrival: Sessions begin promptly—arrive early or risk being denied entry and potentially forfeiting your exam fee.

Food, drink, and study materials: These are not permitted in the testing environment.

Not following instructions: Proctors enforce exam-security rules strictly.

Identification & Name-Match Policies: Your Non-Negotiable Entry Ticket

Your photo ID is your passport into the exam. The DRE is explicit about what is accepted and what is not.

What you must present

You must show one valid, original, government-issued photo ID from the authorized list:

A current state-issued driver’s license or DMV identification card.

A valid U.S. Passport (or a passport issued by a foreign government).

A valid U.S. Military identification card.

The critical name-match reality

Your registration and application must be under your legal name. Common friction points that lead to entry denial include:

Middle Names: Middle initial on one document vs. full middle name on another.

Life Changes: Marriage/divorce name changes not reflected consistently across your documents.

Shortened Names: Using nicknames like “Mike” vs. the legal name “Michael.”

Pro-Tip: If your identity cannot be verified cleanly against the roster, proctors may deny entry. Reconcile any discrepancies at least two weeks before your exam date.

For a full breakdown of documentation and common mismatch fixes, see Identification Requirements for the CA Exam.

Security Screening & Personal Belongings

Knowing the “logistics of the lobby” reduces day-of stress. Here is the standard flow at many exam sites:

Check-in: A proctor verifies your ID and matches you to the roster.

Storage: You will be directed to store personal belongings (typically in lockers, or a designated storage process if lockers are limited).

The Phone Rule: Phones must be powered off and stored as directed. Possession or use of a phone during the exam session—including during breaks—can lead to immediate disqualification.

Final Entry: Once cleared of personal items, you will be assigned a seat.

Best practice: Leave valuables at home or secured in your vehicle. Bring as little as possible to the site.

Prohibited Items: What Not to Bring

The DRE maintains an “Examination Control Information” list. Bringing prohibited items into the testing room can lead to immediate disqualification.

Category

Prohibited Items

Electronics

Cell phones, smartwatches, fitness trackers, tablets, laptops, cameras/recording devices.

Personal Items

Purses, wallets, keys, backpacks, briefcases, suitcases.

Stationery

Your own pens/pencils, paper, notes, flashcards.

Accessories

Hats/caps, lapel pins, tie tacks, smart glasses.

Consumables

Food, drinks/water bottles, gum, and candy.

"Bring Less, Bring Right" Checklist

To ensure a frictionless check-in, only have these items on your person when you approach the proctor:

Your valid, original government-issued photo ID.

Your car key (if not attached to a bulky keychain).

A light sweater or jacket (testing rooms can be chilly).

If you want the “positive list” of what to bring (so you don’t over-pack), read What to Bring to the California Real Estate Exam.

Timing Rules: Arrival, Late Policy, and Breaks

Arrival: Plan to arrive at least 30 minutes early to allow time for check-in, storage, and security.

Late policy: If you arrive after the session has started, you may be denied entry and required to reschedule (which can mean losing your slot and paying again).

Breaks: The exam is a continuous sitting. If you step out for any reason, assume your exam clock continues and follow the proctor’s procedure.

Test-Day Conduct: Disqualification & “Don’t Do This”

To protect exam integrity, follow these rules:

No communication: Don’t speak to or signal other candidates.

No copying: Don’t look at other screens or attempt to reconstruct questions to share later.

Absolute compliance: Follow proctor instructions immediately and without argument.

Violations can result in the exam being terminated and may affect future licensing applications.

Special Situations: Accommodations and “What If…”

Testing accommodations: If you need accommodations (e.g., extra time), you must request and receive approval through the official DRE process well before your exam date.

Medical/comfort aids: Items like insulin pumps or braces may require advance notice for screening—handle this early.

If you are turned away: Don’t panic. Fix the underlying issue (renew ID, correct name mismatch, etc.) and follow our recovery plan in What Happens If You Fail the CA Real Estate Exam.

Final Exam Day Checklist & Next Steps

If you follow these rules, you’ll clear check-in smoothly and can spend your mental energy on the exam itself.

If you pass, read: What Happens After You Pass the CA Real Estate Exam

For the complete roadmap and context, visit the: California Real Estate Exam Guide

Frequently Asked Questions (FAQ)

1. Can I wear a watch during the exam?

No. Watches (including smartwatches) are commonly prohibited. Plan to rely on the on-screen timer.

2. Can I bring my phone if it stays in the locker?

Yes, but it must be powered off and stored exactly as instructed. Do not access it during breaks.

3. What if my ID expired yesterday?

You will likely not be admitted. Your ID must be valid on the exam date.

4. Can I bring my own calculator?

Typically no. There is no longer any math on the California real estate exam and the testing sites no longer provide calculators or dry erase boards.

5. How early should I arrive?

At least 30 minutes before your scheduled start time.

|

You’ve spent weeks—maybe months—memorizing agency relationships, trust fund accounts, and the intricacies of California land use. You are ready to pass the real estate test. But for many candidates, Read more...

You’ve spent weeks—maybe months—memorizing agency relationships, trust fund accounts, and the intricacies of California land use. You are ready to pass the real estate test. But for many candidates, the biggest obstacle isn't the exam questions; it’s the person standing at the check-in desk.

In my 20-plus years of coaching students at ADHI Schools, I’ve seen incredibly well-prepared candidates get turned away before they even touch a keyboard.

Why?

Because of a simple identification mismatch. This guide is your "proctor-proof" checklist to ensure your ID and records are in perfect alignment.

What is the acceptable ID for the CA real estate exam?

According to the California Department of Real Estate (DRE), you must present a valid, current form of photo identification. Only the following are typically accepted: a current state-issued driver’s license or DMV ID card, a U.S. Passport, a foreign government passport, or a U.S. Military ID. You will not be admitted without one of these specific physical documents.

What happens if my name doesn't match my exam ID?

If the name on your photo ID does not match the name on your exam registration, you may be denied entry. While minor formatting differences like a middle initial could be fine, significant discrepancies—such as nicknames or unrecorded name changes—require you to update your DRE record before your exam date to avoid being marked as a "No Show."

The Core Rule: Validation and Alignment

The absolute "Golden Rule" for exam day is that your identification must be current (valid) and it must match the name on your exam registration. The DRE is the final authority on these policies, and testing center proctors follow their handbook strictly. They are not authorized to make "judgment calls." While minor formatting differences are sometimes accepted, you should assume strict matching is required and resolve any discrepancies weeks before your date.

Name Mismatch Risk Assessment

Scenario

Risk Level

Recommendation

Middle Initial vs. Full Middle Name

Low

Usually fine, but full name is the safest bet.

Two Last Names / Spacing (e.g., De La Cruz)

High

Spacing must match your ID exactly.

Accents / Special Characters (José vs Jose)

Medium

Usually system-normalized, but confirm your portal entry.

Nickname (e.g., "Bobby" instead of "Robert")

High

You must update your DRE record to match your ID.

DRE-Aligned Acceptable ID Types

To be admitted into the examination, you must show a valid form of photo identification. Per current DRE guidelines, only the following forms are accepted:

Current state-issued driver’s license

DMV identification card

U.S. Passport

Passport issued by a foreign government

U.S. Military identification card

Important: The DRE is the source of truth for these policies. Always review the most recent "Taking the Exam" guidance from the DRE website before your scheduled date.

High-Risk Situations: Why People Get Sent Home

1. The Expired ID Trap

Even if it only expired yesterday, an expired ID is invalid for testing purposes.

The Fix: Check your expiration date at least 30 days before your exam.

The Risk: You will likely be forced to reschedule and pay a new exam fee.

2. Temporary or Paper IDs

A temporary or paper receipt from the DMV is often not accepted as a primary form of ID because it lacks the required security features of a plastic card.

The Guardrail: If you are waiting on a new license, the safest backup is a valid U.S. Passport that matches your registration exactly. Do not rely on a paper extension unless you have confirmed it meets current testing center compliance.

3. Damaged or Unreadable ID

If your photo is peeling, the plastic is cracked through your name, or the card is heavily worn, a proctor may reject it. If your ID is in poor condition, replace it now.

The 14-Day "Proctor-Proof" Checklist

Two weeks before your exam, perform this final audit:

Confirm Registered Name: Log into the DRE eLicensing portal. Does the name there match your photo ID character-for-character?

Check ID Expiration: Is your ID valid through the date of your exam?

Verify SSN/ITIN Submission: Double-check your initial application records for any typos in your identification numbers.

Locate a Backup ID: If your primary ID is damaged or nearing expiration, ensure your Passport is ready and available.

Print Your Notice: Have your Exam Schedule Notice/confirmation email printed and ready.

What If You Are Turned Away?

If a proctor denies you entry due to an ID issue, you may be marked as a "No Show." This typically means you forfeit your exam fee and must wait for the DRE to process the status before you can reschedule.

If this happens, stay calm. Visit our guide on What Happens If You Fail the CA Real Estate Exam—the process for rescheduling due to a "No Show" is essentially the same as a traditional failure.

To ensure you don't run into other procedural hurdles, be sure to review our comprehensive list of California Real Estate Exam Rules & Testing Policies.

Moving Toward Your License

Being familiar with the check-in process and knowing what to bring to the exam is critical. By having a look at your ID today, you remove the "what-ifs" from exam day. Once you get that "Congratulations" printout at the desk, find out What Happens After You Pass the California Real Estate Exam to finish your journey.

For a complete look at the application process, scheduling, and study strategies, visit our California Real Estate Exam Guide.

|

The “Order of Operations” Confusion

The path to a California real estate license is often clouded by outdated advice, social media "gurus," and aggressive brokerage recruiting scripts. This creates Read more...

The “Order of Operations” Confusion

The path to a California real estate license is often clouded by outdated advice, social media "gurus," and aggressive brokerage recruiting scripts. This creates a massive point of confusion: many aspiring real estate professionals believe they must be "hired" before they can even apply for the state exam.

Mistaking this sequence leads to lost momentum and unnecessary procedural errors.

The typical order is: pre-license school → exam application → passing the state exam → license number issuance → brokerage affiliation.

In my 20+ years of guiding thousands of students at ADHI Schools, I’ve seen this confusion cause more delays than the exam itself. This guide provides the exact roadmap to avoid those traps.

Do You Need a Broker to Apply for a California Real Estate License?

No—you don’t need a broker to apply for or take the California real estate exam. You can complete the education and application without a sponsoring broker affiliation. But you can’t legally practice real estate or earn commissions until your license is placed with a supervising brokerage.

Do You Need a Broker to Take the California Real Estate Exam?

Absolutely not. The Department of Real Estate (DRE) allows any individual who has met the 135-hour education requirement to sit for the exam. You are applying as an individual, not as a representative of a firm. You can take the exam as an individual, regardless of brokerage affiliation.

The Correct California Timeline: A Step-by-Step Roadmap

Following the state-mandated order of operations is the only way to ensure you don’t waste time.

Complete Your 135 Hours of Pre-License Education: You must finish three college-level courses. Can You Take the Exam Before Completing All 135 Hours? No—you must have your certificates in hand first.

Apply for the State Exam & Submit Fingerprints: You submit your application and Live Scan fingerprints to the DRE. You do not need a broker’s signature for the exam application.

Note: The biggest avoidable delays are simple mismatches—your name, ID, and course certificates must match exactly.

Pass the California Real Estate Salesperson Exam: This is your primary hurdle.

Receive Your License Number from the DRE: The DRE issues your license number after clearing criminal background. You can complete this entire process independently and without broker affiliation.

Affiliate with a Brokerage to Practice (“Hang Your License”): Once you have a license number, you must place your license with a supervising broker so you can legally practice and earn commissions.

Pro Tip: If you want the full start-to-finish roadmap, use our California Real Estate License Guide.

Key Terms Demystified

Understanding DRE terminology prevents "bureaucratic paralysis."

“Applying for a License” vs. “Practicing”: Applying is between you and the State. Practicing is between you and a Broker. You can do the first without the second.

“Hanging/Placing Your License”: This means officially associating your license with a Broker of Record. This is what moves your license into a status that allows for commissions.

Independent Contractor Reality: You are a 1099 contractor. The broker supervises your licensed activity; however, you generate your own business unless the brokerage specifically provides leads.

What Happens After You Get Your California Real Estate License? The focus shifts from "passing the test" to "building a business."

When (and Why) to Talk to Brokerages Early

Research is smart; commitment is premature. You should interview brokerages while you wait for your exam date to assess:

New Agent Training: Does the broker have a formal mentorship program?

Commission Splits & Fees: What is the actual "take-home" after all fees?

Lead Generation Support: Do they provide leads or just "coaching"?

Compliance Support: Who reviews your contracts to keep you out of court?

Costly Mistakes to Avoid

Waiting to Apply Until You Find a Broker: I’ve watched students wait 90 days "shopping brokerages" while their exam eligibility window and motivation evaporated. Don't wait. Apply the moment you have your certificates.

Choosing a Brand Over Training: I once spoke to an agent who picked a famous global brand for the "vibe," but quit after 4 months because no one showed them how to actually get business. Top Reasons People Fail to Get Licensed in California often trace back to a lack of early support.

Losing Momentum After the Exam: The gap between passing the exam and finding a broker should be days, not months.

Your 7-Day Action Plan

Day 1-2: Finish your current education course module.

Day 3: Draft a shortlist of 3-5 local brokerages to research.

Day 4: Prepare 8 questions to ask future brokers (focus on training and splits).

Day 5: Double-check your DRE exam/license application for errors (name match, IDs, and certificates).

Day 6-7: Submit your application to the DRE.

Frequently Asked Questions (FAQ)

Can I apply for the CA real estate exam without a brokerage?

Yes. Affiliation is not required to apply for or take the exam.

Do I need a sponsor broker for the exam?

No. Sponsoring brokers are required for practicing, not for taking the exam.

Can I interview brokerages before I’m licensed?

Yes, and you should. Most brokers are happy to speak with prospective agents who are currently in school.

What if I join a brokerage now—does it speed up the DRE?

No. The DRE processes applications in the order received, regardless of which brokerage you intend to join.

What if I pass the exam but don’t pick a brokerage?

You will have a license number, but you cannot legally represent clients or collect a penny in commission until you associate your license with a broker.

Can my license expire if I don’t join a brokerage right away?

Your license remains valid once issued, but you must still meet renewal requirements and continuing education deadlines every four years, regardless of whether you are affiliated with a broker.

Next Steps on Your Licensing Journey

The brokerage choice is critical for your success in the field, but it is not a prerequisite for the state exam. Focus on your 135 hours and your application first.

For the complete, step-by-step licensing roadmap (start to finish), use our California Real Estate License Guide.

|

If you're gearing up for your California licensing test, one of the most practical details to lock down is the exam's length. How many questions are on the California real estate exam? Knowing the exact Read more...

If you're gearing up for your California licensing test, one of the most practical details to lock down is the exam's length. How many questions are on the California real estate exam? Knowing the exact number is the cornerstone of an effective study plan and confident test-day pacing. Here’s the straightforward answer:

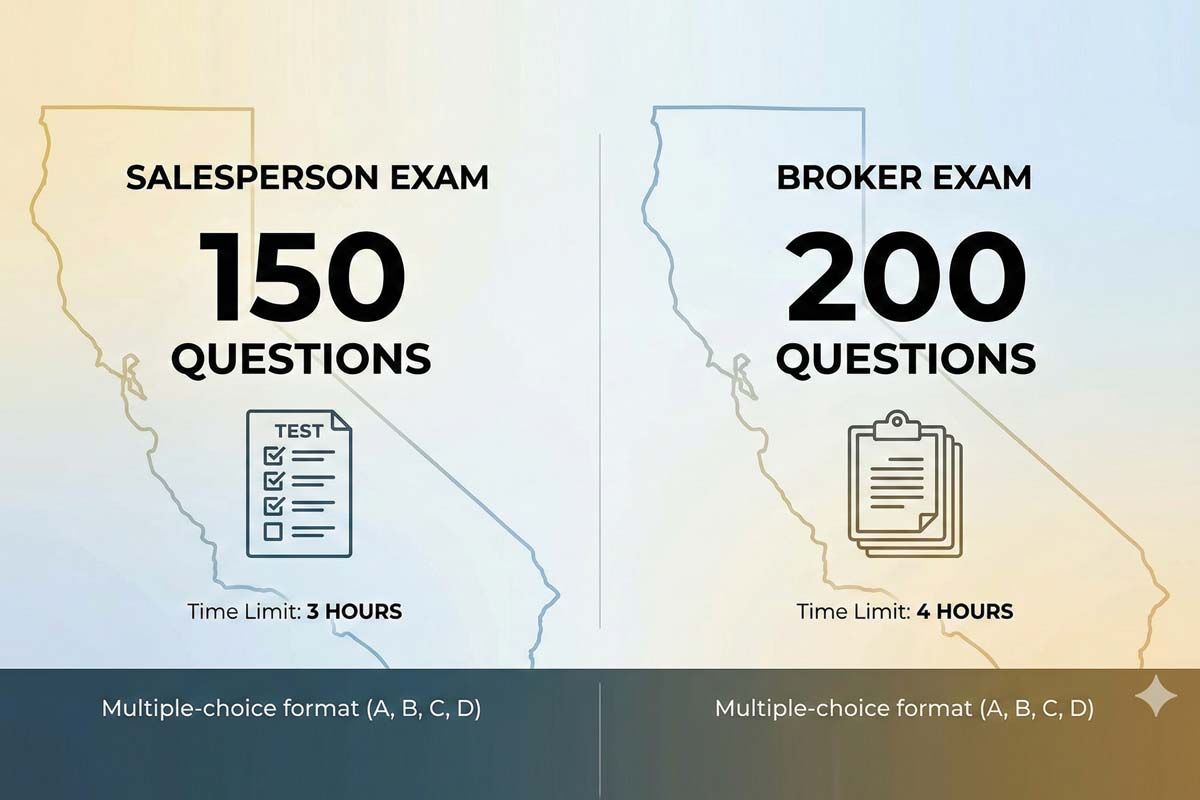

The California Real Estate Salesperson Exam contains 150 multiple-choice questions.

The California Real Estate Broker Exam contains 200 multiple-choice questions.

This structure directly influences your time-management strategy. For a full picture of the entire testing process, from scheduling to scoring, our California real estate exam guide walks you through every step. To see how these questions are distributed by topic, review our guide to what’s on the California real estate exam — it outlines all testable areas.

The Salesperson Exam Breakdown (150 Questions)

The salesperson licensing exam is a 150-question test, with every item presented in a multiple-choice format with four options (A, B, C, D). The questions are pulled from specific content areas with predetermined weighting. For example, roughly a quarter of the exam focuses on the Practice of Real Estate and Duties to Clients, while Financing makes up a smaller percentage. Understanding this weighting is critical for efficient study.

The Broker Exam Breakdown (200 Questions)

The broker exam increases in both scope and depth, featuring 200 multiple-choice questions, also in A, B, C and D format. While the core subject categories align with the salesperson test, the broker version delves slightly deeper into areas like real estate law, brokerage management, and trust fund handling. The additional questions reflect the content around supervisory knowledge required for a broker's license.

Time Management: The “Minute-Per-Question” Rule

With standardized time limits, a simple calculation gives you a powerful pacing tool:

Salesperson Exam: 150 questions / 180 minutes = 1.2 minutes per question.

Broker Exam: 200 questions / 240 minutes = 1.2 minutes per question.

This consistent pace is very manageable if you avoid getting stalled. The best approach is to answer known questions quickly, mark uncertain ones for review, and maintain forward momentum. Returning to challenging items at the end ensures you capture all the points available from questions you find easier.

Passing Scores: How Many You Can Get Wrong

It’s a relief to many students that perfection is not required. The passing percentages are clear:

Salesperson Exam: A 70% score means you need 105 correct answers. You can miss 45 questions and still pass.

Broker Exam: A 75% score requires 150 correct answers, allowing you to get 50 questions wrong.

This margin for error is built into the exam design. For a deeper look into the scoring process, including how "equating" questions work, our article on how the California real estate exam is scored provides clarity.

Format Consistency: Every Question Is Multiple Choice

Since the exam sticks to a simple four-option multiple-choice format, you don’t have to adjust your thinking from question to question. Learn one solid strategy and you can use it throughout the test—whether you know the answer or you’re narrowing it down to the best option. Honing this skill is a major part of effective preparation, and a dedicated multiple-choice strategy for the CA real estate exam can significantly boost your confidence and accuracy.

So, to recap: the sales license exam has 150 questions, and the broker test has 200 questions. When you understand the question count, timing, and pass thresholds, the exam stops feeling mysterious and becomes a numbers game you can win. With focused study and smart test-taking tactics, you’re well-positioned for success. For a complete step-by-step journey to your license, your central reference should always be our main California real estate exam guide.

Frequently Asked Questions

Q: Is there math on the California real estate exam? A: No. Since calculators are strictly prohibited, the DRE has removed math calculation questions from the test. You may need to recall specific numbers (like knowing there are 43,560 square feet in an acre), but you will not be asked to perform arithmetic.

Q: Do all 150 questions count toward my score? A: Treat every question as if it counts. While the DRE may include a few unscored "experimental" questions to test them for future exams, they are not labeled.

Q: Is the Broker exam harder than the Salesperson exam? A: Yes, primarily due to endurance. Answering 200 questions over 4 hours is a mental marathon. It also tests supervisory topics that aren't on the salesperson exam.

Q: What happens if I don't finish in time? A: Any blank answer is marked wrong. There is no penalty for guessing, so if you are running out of time, pick a letter and fill in every remaining bubble before the clock stops.

|

Deep knowledge of real estate principles is non-negotiable. However, even the most dedicated students can stumble if they rely on memorization alone.

That’s because the Department of Real Estate (DRE) Read more...

Deep knowledge of real estate principles is non-negotiable. However, even the most dedicated students can stumble if they rely on memorization alone.

That’s because the Department of Real Estate (DRE) isn’t simply checking your memory; the exam tests your professional judgment. They want to ensure you can protect a client in a complex scenario. To pass, you need to combine your command of the facts with a clear understanding of how the exam measures critical thinking.

This article teaches you how to think like the DRE—because passing is as much about mental process as it is about content.

What You Will Learn

The "Best Answer" Logic: Why two answers can be right, but only one aligns with DRE scoring.

The Keyword Radar: How to spot trap words like "Always" and "Must" that signal incorrect answers.

Scenario Mastery: How to filter out the irrelevant "noise" in complex story problems.

Psychometric Hacks: How to mathematically increase your guessing odds from 25% to 50%.

This article is the strategic companion to our California Real Estate Exam (2026 Complete Guide). If that guide is your roadmap, this article is your instruction manual for driving the car.

How to Outsmart DRE Multiple-Choice Logic

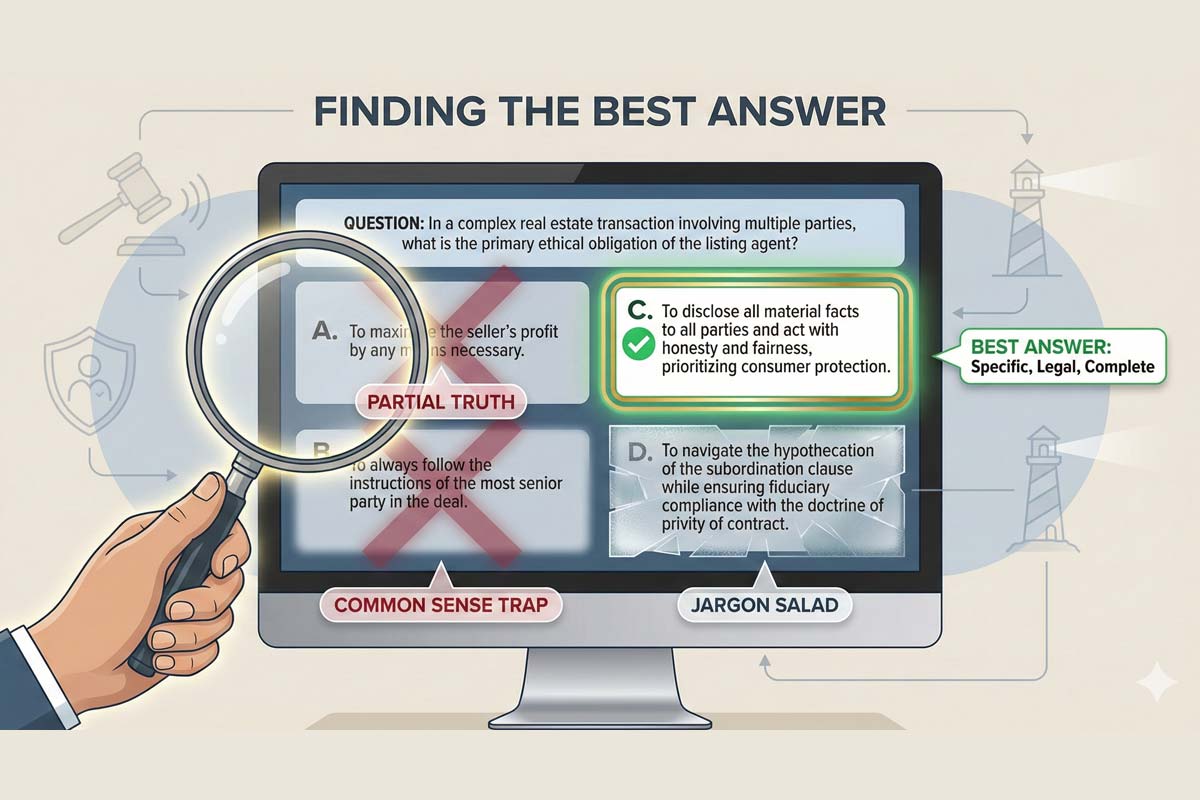

To beat the exam, you have to deconstruct the weapon formed against you. The DRE does not write random questions; they write questions that follow a specific hierarchy of correctness.

The “Best Answer” Theory

If you take nothing else from this article, take this: In the DRE world, correct is not enough.

This is where smart people fail. They read option (A), see that it is technically a true statement, mark it, and move on. They never read option (C), which was more specific or more applicable to the exact scenario described.

Insider Insight: The DRE almost never rewards the answer that is merely technically accurate—they reward the one that aligns with legal intent and consumer protection.

Insider Tip: Never mark an answer until you have read all four choices. Often, option (A) is a "Partial Truth"—a statement that is true in a vacuum but doesn't solve the specific problem in the question stem.

When Two Answers Look the Same

This is the #1 anxiety point for students. You will see two answers that both look "right." Usually, the difference comes down to scope.

Broad vs. Specific: If the question asks about a specific violation (e.g., commingling), the answer that cites the specific code or action is better than the answer that just says "unethical behavior."

The Scope Mismatch:

Question: "What is the primary duty of a property manager?"

Choice A: To keep the building fully occupied.

Choice B: To generate the highest net income consistent with the owner's objectives.

Analysis: Choice A is good. Choice B is better because it encompasses the owner's goals, not just occupancy. The DRE rewards precision.

Anatomy of a DRE Question

Let’s break down the components of the items you’ll face.

1. The Stem

This is the setup. It might be a direct question (“What is an easement?”) or a scenario (“Broker Bob lists a property…”).

Insider Tip: Read the last sentence of the stem first. This tells you exactly what they are looking for before you get bogged down in the story details.

Clarification: This is a preview technique. Once you know the goal, you must still read the full scenario. Do not skip the middle, or you will miss the twist.

2. The Distractors (The Traps)

These are the wrong answers. They aren’t random; they are designed to trap you.

The "Common Sense" Trap: An answer that sounds logical to a layperson but violates real estate law.

Example: "The broker should return the deposit because the buyer is sad." (Kind, but legally wrong).

The "Jargon Salad": An answer that throws in impressive words just to intimidate you.

Example: "The hypothecation of the subordination clause." (If it sounds like nonsense, it usually is).

Scenario-Based Question Mastery

Now that you understand distractors, let’s look at the DRE’s favorite testing style: long scenario questions.

The DRE loves to test whether you can separate signal from noise. They will give you a paragraph full of details, but often only one fact matters. This is why it’s important to not only understand the content of the real estate exam but also how to cut through the fluff to get to what the state is actually asking.

The "Red Herring" Technique:The exam writers will include facts that have nothing to do with the legal issue.

Example: "A buyer looks at a Victorian home built in 1977. It is painted blue, has a large swimming pool, and the seller is going through a messy divorce..."

The Trap: You focus on the pool, the color, or the seller's emotional state.

The Reality: The year "1977" is the only thing that matters (Lead-Based Paint Disclosure).

Beware of Details That Seem Important but Aren't :

Exact square footage.

Emotional descriptions ("distressed seller," "anxious buyer").

"Curb appeal" descriptions.

Rule: If the detail doesn't change the legal outcome, ignore it.

The Keyword Radar System

The English language is flexible. The law is not. The DRE uses specific qualifiers to signal whether an answer is likely right or wrong.

The "Always" and "Never" Trap (Absolutes)

Real estate is rarely black and white. There are exceptions to almost every rule. If you see these words, the answer is highly likely to be incorrect:

Always

Never

Must

Everyone

Example: "A broker must disclose a death on the property." (False. You only must disclose it if it occurred within 3 years or if the buyer asks. The absolute "must" makes this answer incorrect).

The Exception: When the law deals with Fair Housing, "Never" is often correct. You never discriminate based on race.

The "Generally" and "Most" Safety Net (Conditionals)

The DRE prefers answers that leave room for nuance. If you are forced to guess, these words often signal the correct answer:

Generally

Typically

Most likely

May

Example: "The agent must generally obey the client." (Safe, accurate, allows for exceptions).

The Skip-and-Return Strategy

Based on the number of questions on the real estate exam, it’s evident that time management is crucial. You have roughly 1.2 minutes per question on both the sales and broker exams.

Do not let your ego lose you points.

If you encounter a scenario question that is a paragraph long: Mark it for review and skip it.

Momentum: Answering 10 easy questions in a row builds confidence.

Subconscious Processing: Your brain will continue to work on the hard question in the background.

Process of Elimination (POE)

If you don’t know the answer, you can still manufacture a higher probability of passing.

Psychometricians intentionally design four-option items with two distractors that are easy to eliminate—because this increases reliability and makes POE mathematically powerful.

Blind Guess: 25% chance of success.

Eliminating 2 Distractors: 50% chance.

The Math of Passing: As detailed in our guide on How the California Real Estate Exam Is Scored, you need a 70% to pass. That means you can miss 45 questions. If you can use POE to get your guessing success rate up to 50% on the hard questions, you are mathematically on the path to passing.

Full-Question Reading Discipline

Speed is your enemy. The DRE writes questions that pivot in the middle.

The "Except" and "Not" Twist

The DRE loves negative stems:

"All of the following are necessary for a valid contract, EXCEPT..."

If you read too fast, your brain skips "EXCEPT." You mark option (A) because it is necessary, and you fail the question.

Technique: When you see "EXCEPT," mentally rephrase the question: "I am looking for the WRONG statement."

Stop Overthinking (The Anxiety Check)

Most test-takers sabotage themselves by letting adrenaline override logic—strategy is how you stay in control.

The Exam is Not Evil: It is designed to assess competence, not to prank you.

Trust Your First Instinct: Once you have used the Process of Elimination, your first instinct is statistically more likely to be correct. Second-guessing without new information usually leads to changing a right answer to a wrong one.

Default to Safety: If you are stuck, ask yourself: "Which answer best protects the consumer?" That is usually the direction the DRE wants you to go.

The 2026 Angle: What Has Changed?

While the core mechanics of multiple-choice psychometrics remain consistent, the DRE updates its exam with some regularity to ensure that the content of the real estate exam reflects the reality of the real estate landscape.

In 2026, we are seeing a continued emphasis on ethics and transparency.

What to Expect:

Scenario Questions: Testing whether you recognize when a disclosure is required or when a duty to a non-client arises.

Fair Housing Granularity: Expect questions that drill down into subtle discrimination, not just obvious bias.

Agency Duties: A shift away from "closing the deal" toward "fiduciary transparency."

Key Exam-Day Takeaways

Read the last sentence first to identify the goal of the question.

Eliminate absolutes (Always/Never) unless it's a Fair Housing question.

Identify the scope: If the question is specific, the answer must be specific.

Don't over-read: If the fact isn't in the paragraph, it doesn't exist.

Apply these four rules, and the exam becomes a formality rather than a hurdle.

Strategy is vital, but it cannot replace content mastery. You need to combine these test-taking tactics with a comprehensive study plan.

Start with the full roadmap here: California Real Estate Exam (2026 Complete Guide).

Inside, you'll find the complete content breakdown, registration steps, preparation timelines, and scoring explanations you need to pass on the first try.

FAQ: Cracking the DRE Code

Q: What is the "Best Answer" strategy for the CA Real Estate Exam?

A: "Best Answer" logic means ignoring options that are merely true and selecting the one that is most specific to the scenario. Based on how the DRE scores the exams, while two answers could “look” correct, choose the one that aligns with consumer protection and specific legal intent rather than a broad generalization.

Q: Are there specific "trap words" that signal a wrong answer?

A: Yes. Be suspicious of absolute words like "Always," "Never," "Must," and "Everyone." Since real estate law almost always has exceptions, these are usually incorrect. Exception: In Fair Housing questions, "Never" discriminate is often the right answer.

Q: How do I handle long, confusing scenario questions?

A: Use the "Last Sentence First" technique. Read the very end of the question prompt before reading the story. This tells you exactly what legal issue to look for so you can filter out "noise" like emotional descriptions or irrelevant house details.

Q: How can I improve my odds if I have to guess?

A: Use Process of Elimination (POE). The DRE includes two "distractors" (obvious wrong answers) in almost every question. By crossing these out, you mathematically double your chance of guessing correctly from 25% to 50%.

Q: What is the "Red Herring" technique on the exam?

A: A Red Herring is an irrelevant fact designed to distract you. For example, a question about Lead-Based Paint might mention a "messy divorce." The divorce is the Red Herring; the year the house was built is the only fact that matters.

Q: How should I handle "EXCEPT" or "NOT" questions?

A: These negative stems cause high failure rates due to speed reading. When you see "EXCEPT," mentally rephrase the question to: "I am looking for the FALSE statement." This prevents you from accidentally marking the first true statement you see.

|

The California real estate exam isn’t a secret code you have to crack in order to pass. The DRE actually publishes a blueprint that tells the world exactly what’s on the test. Once you know how the Read more...

The California real estate exam isn’t a secret code you have to crack in order to pass. The DRE actually publishes a blueprint that tells the world exactly what’s on the test. Once you know how the questions are weighted, you can stop wasting time and start studying the right way and focusing on the things that matter.

I’m going to map it all out for you below.

But first, here is some good news: the biggest section on the exam isn’t necessarily the hardest one.

If you are just beginning your licensing journey, start with our comprehensive California real estate exam guide for a full roadmap.

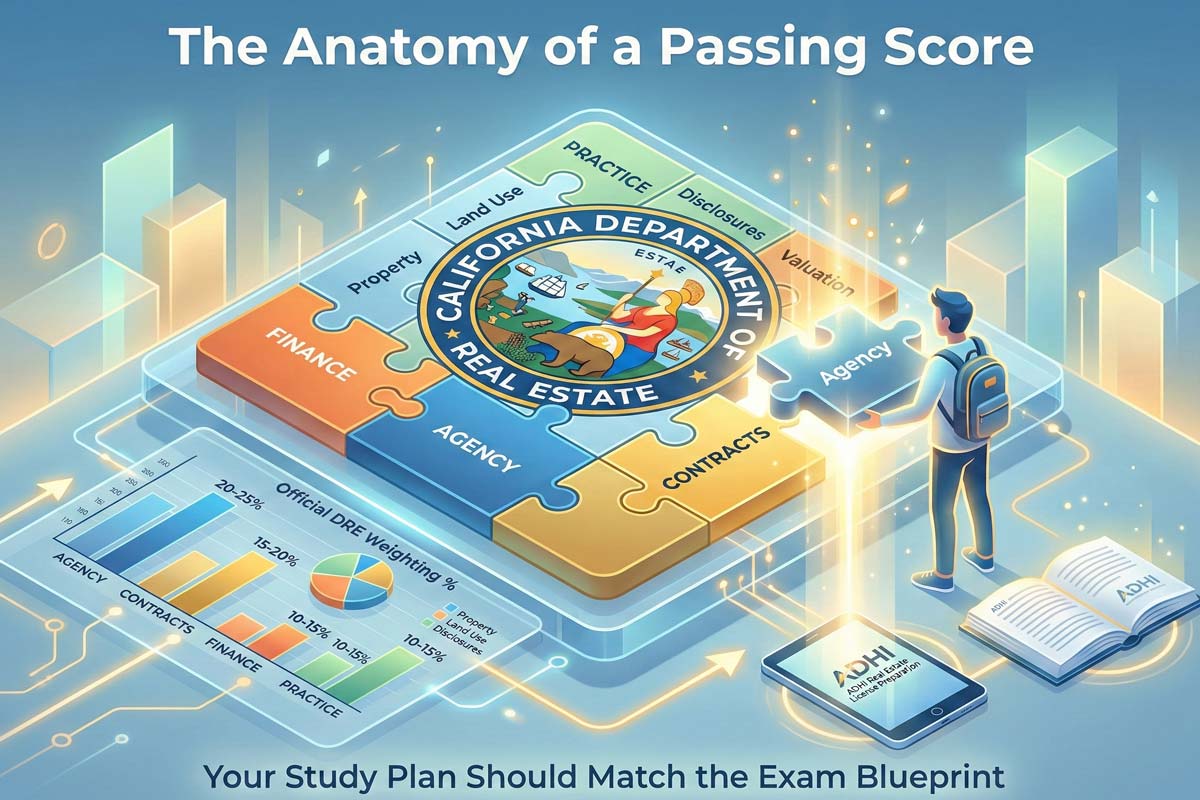

The 7 Major DRE Exam Categories

The DRE divides the exam into seven competency areas. While the official titles can sound academic, it is easier to understand them as the practical responsibilities of a licensee.

Property Ownership and Land Use Controls and Regulations: This tests your knowledge of what you are selling—the rights, interests, and restrictions attached to the land.

Laws of Agency and Fiduciary Duties: This covers who you represent and the legal obligations you owe to your clients.

Property Valuation and Financial Analysis: This requires you to understand how value is determined and how investment properties are analyzed.

Financing: This covers the systems, laws, and instruments used to borrow money for real estate.

Transfer of Property: This tests the mechanics of how ownership moves from one person to another (deeds, escrow, and title).

Practice of Real Estate and Mandated Disclosures: This is the "day-to-day" work of an agent, including fair housing, truth-in-advertising, and trust funds.

Contracts: This covers the agreements that make the transaction legally binding.

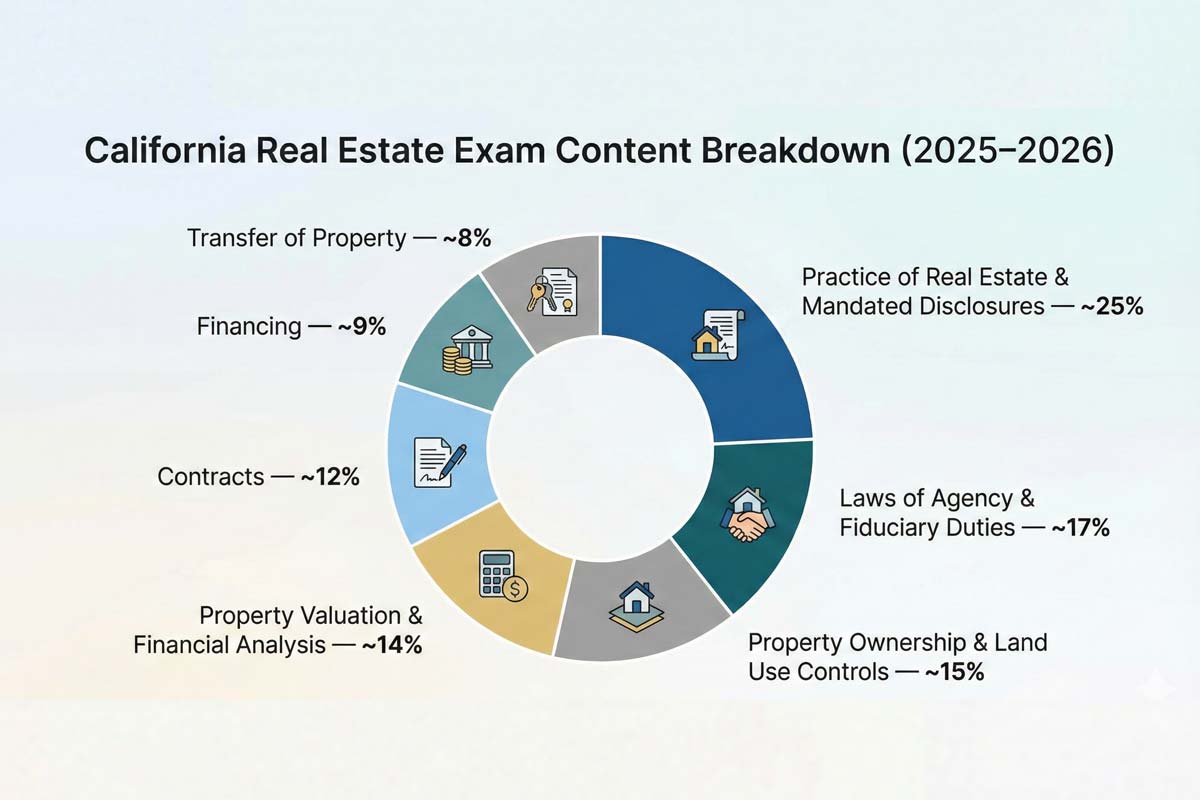

Which exam category is worth the most points? The Practice of Real Estate and Mandated Disclosures is the heavyweight champion of the exam, accounting for roughly 25% of the questions. However, as we will discuss below, this category is actually a mix of several different skill sets.

These seven categories are the standard framework for both the salesperson and broker exams.

Category-by-Category Weighting (2025–2026)

The DRE provides a percentage range for each topic. Below, we break down these weights into a practical study guide.

Practice of Real Estate and Mandated Disclosures (~25%)

What It Really Covers: This is the largest section of the exam. It includes Trust Fund handling, Fair Housing laws (Federal and State), the purpose of the Transfer Disclosure Statement (TDS), and strict rules regarding advertising and ethics.

Instructor’s Study Tip: Do not be intimidated by the 25% figure. This category is not one giant topic; it breaks down between disclosures, ethics, fair housing and general real estate practice scenarios. If you master Fair Housing and the rules of Trust Funds (commingling and conversion), you have conquered the hardest part of this section.

Laws of Agency and Fiduciary Duties (~17%)

What It Really Covers: This tests how agency is created (express vs. implied), how it is terminated, and the specific duties owed to principals versus third parties. It heavily features "dual agency" scenarios.

Instructor’s Study Tip: Focus on the timing of the Agency Disclosure Form (Disclosure, Election, Confirmation). The DRE loves to test on when these disclosures must happen in a transaction sequence.

Property Ownership and Land Use Controls (~15%)

What It Really Covers: This covers the different ways to hold title (Joint Tenancy, Community Property), encumbrances (liens, easements), and government powers (Zoning, Eminent Domain).

Instructor’s Study Tip: Understand the "Bundle of Rights." Many questions here are definition-heavy. If you know the difference between a specific lien and a general lien, you can pick up easy points here.

Property Valuation and Financial Analysis (~14%)

What It Really Covers: This is about appraisal theory (Cost, Income, and Market Data approaches) and economic principles of value (Substitution, Contribution).

Instructor’s Study Tip: Don't worry about complex math. The exam tests concepts, not calculations. Focus on knowing when to use the Income Approach (commercial/rentals) versus the Cost Approach (libraries/new schools).

Contracts (~12%)

What It Really Covers: This section deals with the validity of contracts (Competence, Mutual Consent, Lawful Object, Consideration) and the specific types of listings (Exclusive Right to Sell vs. Exclusive Agency).

Instructor’s Study Tip: Memorize the four essentials of a valid contract. Also, ensure you understand the "Safety Clause" in listing agreements—it’s a frequent exam target.

Financing (~9%)

What It Really Covers: This covers the primary vs. secondary mortgage markets, loan types (FHA, VA, Conventional), and consumer protection laws like TILA (Reg Z) and RESPA.

Instructor’s Study Tip: This is the smallest section for a reason. Do not spend weeks studying mortgage tables. Focus on the difference between the Trustor, Trustee, and Beneficiary in a Deed of Trust.

Transfer of Property (~8%)

What It Really Covers: This deals with deeds (Grant vs. Quitclaim), title insurance (CLTA vs. ALTA), and the escrow process.

Instructor’s Study Tip: This is often the easiest section to master because it is procedural. If you understand that a deed must be delivered and accepted to be valid (but not necessarily recorded), you are halfway there.

Salesperson vs. Broker Exam Content: What’s Different?

While both exams utilize the exact same seven categories, the lens through which you are tested changes.

The Salesperson exam focuses on the application of rules: "What form do I use?" or "What must I disclose?"

The Broker exam focuses on the above as well as a little more on supervision and management. In addition to the standard content, Broker candidates must understand:

Office management and supervision of salespersons.

Deeper liability regarding Trust Fund accounting.

More complex financial analysis and investment scenarios.

Is the content breakdown the same for salesperson and broker exams? Yes. The DRE uses the same "Content Outline" for both. However, the Broker exam contains 200 questions compared to the Salesperson's 150 and you have to score slightly better on the broker exam to pass.

For more on passing thresholds, read our breakdown of How the California Real Estate Exam is Scored.

How Content Weighting Should Shape Your Study Plan

Do not study every topic with equal intensity. The weighting reveals that the DRE values certain competencies over others.

High-Value vs. Low-Effort Topics

High-Value / High-Complexity: "Laws of Agency" and "Practice of Real Estate" combine for over 40% of your score. These require deep study because they are scenario-based. You cannot just memorize definitions; you must understand how to apply the law to a situation.

Low-Effort / Easy Points: "Transfer of Property" and "Property Ownership" often rely on static definitions (e.g., "What is a freehold estate?"). These are "low-effort" points. Master the vocabulary here to bank easy points, which gives you a buffer for the harder scenario questions.

Which exam topics give you the easiest points? Contracts and Transfer of Property. The rules in these sections are rigid and rarely change, making the questions straightforward if you know your definitions.

How the DRE Uses Weighting to Build and Score the Exam

The DRE uses a psychometric process called "equating" to ensure fairness. Whether you take the exam on a Tuesday in San Diego or a Friday in Oakland, the computer algorithm pulls questions to match this exact percentage blueprint.

Because the DRE uses this fixed blueprint, ADHI Schools’ practice exams mirror the real exam’s balance. When you take our mock tests, you are conditioning your brain to handle the exact distribution of topics you will face on test day.