Most students walk into the California real estate exam feeling confident—until they start wondering how the DRE actually scores it. Is the test curved? Do different people get different versions? Does Read more...

Most students walk into the California real estate exam feeling confident—until they start wondering how the DRE actually scores it. Is the test curved? Do different people get different versions? Does getting exactly 70% guarantee a pass?

Here’s the truth:

The DRE does NOT curve the exam and you can absolutely pass on the first attempt once you understand how their scoring system works.

In this guide, I’ll break down every scoring rule the DRE uses—clearly, accurately, and in plain English—so you know exactly what it takes to pass.

If you’re just getting started, make sure you are also reviewing our full California Real Estate Exam Guide for the complete exam roadmap.

The California Real Estate Exam Scoring System Explained

The most important thing to understand is this:

The California real estate exam uses raw scoring, not curved scoring.

This is the backbone of how the DRE ensures fairness.

Minimum Passing Scores

Salesperson Exam: You must achieve the equivalent of 70%

Broker Exam: You must achieve the equivalent of 75%

Those percentages are absolute—not relative to how anyone else performs.

Why Raw Scoring Makes the Exam Fair

The California DRE uses a raw scoring system to determine a pass or fail. This means your score is based directly on the number of questions you answer correctly, measured against a fixed, non-negotiable threshold.

However, to ensure this raw score is a fair measure for every test-taker, the DRE employs a rigorous process of exam form equating before any candidate ever sees the questions.

What this means for you:

The target is fixed: You must achieve a set number of correct answers.

It is NOT a curve: Your score is never compared to other test-takers on your day. Equating adjusts the exam, not your grade based on others' performance.

In essence, raw scoring gives you a clear target, while expert equating guarantees that hitting that target means the same thing, no matter which exam form you receive.

Debunking the "Scaled Score" Myth

You'll hear many prep courses and forums talk about the DRE's "scaled scoring." This is a widespread misconception. The California DRE does not use a traditional scaled score to determine your pass/fail result.

Here’s the reality:

1. The DRE uses a raw score against a fixed standard.

Your exam is scored on a straightforward, raw percentage basis. To pass, you must correctly answer a specific percentage of questions (approx. 70% for salesperson, 75% for broker). The result is a direct comparison of your correct answers to this absolute benchmark.

2. "Equating" happens before you take the test, not after.

The process often mistaken for "scaling" is called equating. This is a psychometric calibration performed by the DRE during the exam development phase. Experts adjust and validate questions so that the difficulty of reaching the passing raw score is consistent across all exam versions. This means:

You are not compared to other test-takers.

Your score is not statistically manipulated after you finish.

The fairness is built into the exam design itself.

3. The system protects every test-taker.

By using equated exam forms with a raw score threshold, the DRE ensures that:

Every candidate faces an equivalent challenge to demonstrate competency.

No one is penalized for receiving a version with statistically “harder” questions.

The meaning of a "pass" is uniform across the entire state and testing period.

Think of it like a race:

A true "scaled" score might change the finish line based on who's running. The DRE's system, instead, carefully calibrates the track so that everyone runs the same distance to reach the fixed, unmoving finish line. Your raw score simply tells you if you crossed it.

You will NOT receive a numeric score when you pass

The DRE releases only:

PASS

FAIL

When you pass the exam, they do not tell you how close you were or how many you missed.

However, if you fail the exam, the DRE will report your overall score as well as how you did in each of the seven exam categories so you know where to focus your efforts.

Does the DRE Curve the Exam?

Let’s say it as clearly as possible:

No. The California real estate exam is NOT curved.

There is:

No bell curve

No percentile ranking

No grading against other students

How Fast the DRE Scores Your Exam

Since the state exam is computer based you receive your result immediately after finishing.

Important scoring rules

No partial credit

No appeals

No score breakdowns

Pass/Fail only

Retakes

If you fail:

You may retake the exam after paying the re-exam fee

Your previous exam performance has no impact on future tests

Common Myths About Exam Scoring

❌ Myth #1: “Only a certain percentage of students pass each day.”

False.

There is no quota. Passing is based only on your performance relative to the published standard.

❌ Myth #2: “If you test in the afternoon, your exam is harder.”

Completely false.

Versions are pre-set and rotated randomly.

❌ Myth #3: “Different categories are weighted differently for each student.”

Partially true but misunderstood.

The exam blueprint allocates topics by percentage, but every student receives the same category weighting.

Scaling does not adjust category weight per individual.

See our Exam Content Breakdown for exact percentages.

❌ Myth #4: “The DRE tells you your raw score if you call.”

They do not.

No one at the DRE can release that information.

Ready to Pass on the First Attempt?

If you want the highest probability of passing the first time, start with ADHI Schools.

ADHI offers:

California salesperson pre-license courses

Broker licensing courses

Live crash courses taught by real instructors

Exam prep tools that mirror the DRE’s weighting and question style

Our students pass because our test taking strategies are built around how the DRE actually scores the exam—not myths, shortcuts, or generic national content.

Is the California real estate exam curved? No. The California DRE uses a raw scoring system, not a curve. Your score is based solely on the number of questions you answer correctly, and it is never graded against or compared to the performance of other students.

What is the passing score for the California real estate exam? For the Salesperson Exam, you must achieve a score of 70%. For the Broker Exam, the passing threshold is 75%. These percentages are fixed and non-negotiable.

Does the DRE use scaled scoring? No. While the DRE uses a process called "equating" to ensure different versions of the test have the same difficulty level, this happens before you take the test. Your final grade is a simple raw score based on your correct answers, not a statistically manipulated "scaled" score.

Will I see my actual final score? Only if you fail. If you pass, the DRE only releases a "PASS" notification with no numeric score or breakdown. If you fail, you will receive your numerical score and a breakdown of your performance across the seven exam categories.

Is there a limit to how many people can pass each day? No. There is no quota for passing grades. Every single student who hits the required 70% (or 75% for brokers) will pass, regardless of how many other people are testing that day.

How long does it take to get my exam results? You will receive your results immediately. Because the California exam is computer-based, your pass/fail status is provided at the testing center the moment you finish.

Does the time of day affect exam difficulty? No. It is a myth that afternoon exams are harder. Exam versions are pre-set and rotated randomly; the time of day you test has absolutely no impact on which version you receive.

|

The California real estate exam isn’t a secret code you have to crack in order to pass. The DRE actually publishes a blueprint that tells the world exactly what’s on the test. Once you know how the Read more...

The California real estate exam isn’t a secret code you have to crack in order to pass. The DRE actually publishes a blueprint that tells the world exactly what’s on the test. Once you know how the questions are weighted, you can stop wasting time and start studying the right way and focusing on the things that matter.

I’m going to map it all out for you below.

But first, here is some good news: the biggest section on the exam isn’t necessarily the hardest one.

If you are just beginning your licensing journey, start with our comprehensive California real estate exam guide for a full roadmap.

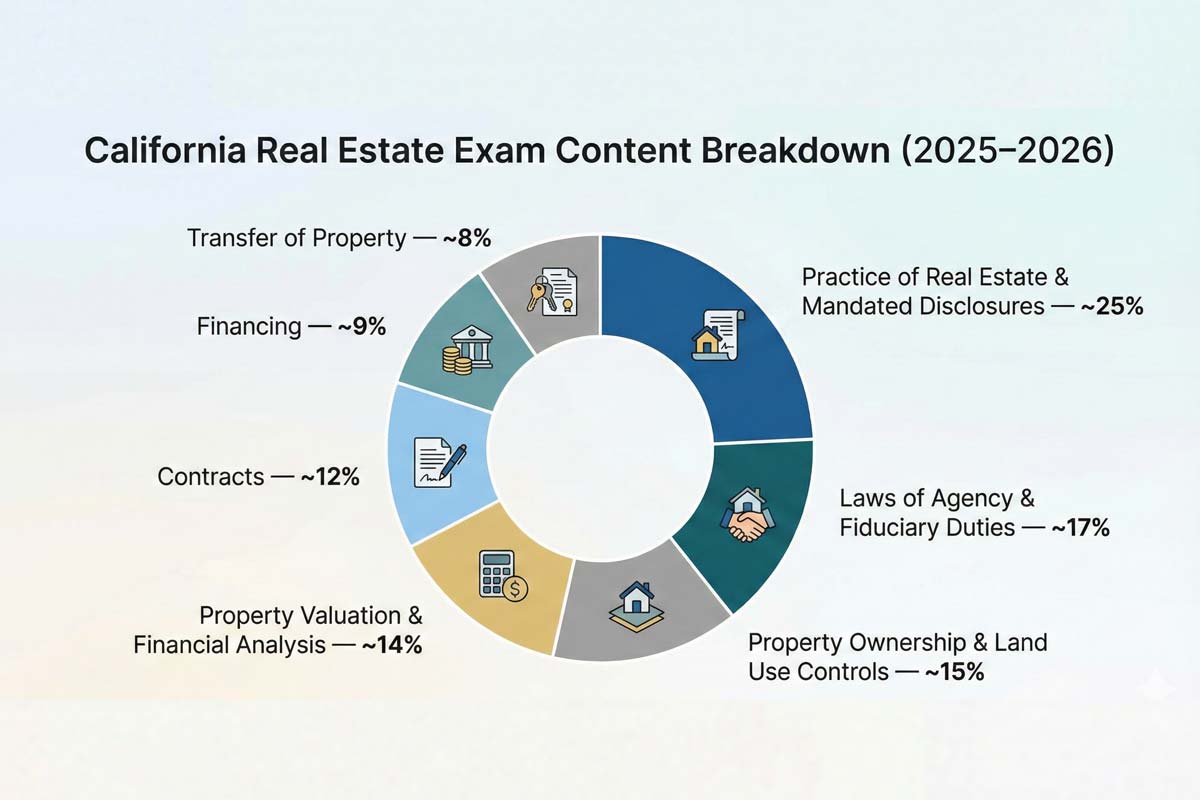

The 7 Major DRE Exam Categories

The DRE divides the exam into seven competency areas. While the official titles can sound academic, it is easier to understand them as the practical responsibilities of a licensee.

Property Ownership and Land Use Controls and Regulations: This tests your knowledge of what you are selling—the rights, interests, and restrictions attached to the land.

Laws of Agency and Fiduciary Duties: This covers who you represent and the legal obligations you owe to your clients.

Property Valuation and Financial Analysis: This requires you to understand how value is determined and how investment properties are analyzed.

Financing: This covers the systems, laws, and instruments used to borrow money for real estate.

Transfer of Property: This tests the mechanics of how ownership moves from one person to another (deeds, escrow, and title).

Practice of Real Estate and Mandated Disclosures: This is the "day-to-day" work of an agent, including fair housing, truth-in-advertising, and trust funds.

Contracts: This covers the agreements that make the transaction legally binding.

Which exam category is worth the most points? The Practice of Real Estate and Mandated Disclosures is the heavyweight champion of the exam, accounting for roughly 25% of the questions. However, as we will discuss below, this category is actually a mix of several different skill sets.

These seven categories are the standard framework for both the salesperson and broker exams.

Category-by-Category Weighting (2025–2026)

The DRE provides a percentage range for each topic. Below, we break down these weights into a practical study guide.

Practice of Real Estate and Mandated Disclosures (~25%)

What It Really Covers: This is the largest section of the exam. It includes Trust Fund handling, Fair Housing laws (Federal and State), the purpose of the Transfer Disclosure Statement (TDS), and strict rules regarding advertising and ethics.

Instructor’s Study Tip: Do not be intimidated by the 25% figure. This category is not one giant topic; it breaks down between disclosures, ethics, fair housing and general real estate practice scenarios. If you master Fair Housing and the rules of Trust Funds (commingling and conversion), you have conquered the hardest part of this section.

Laws of Agency and Fiduciary Duties (~17%)

What It Really Covers: This tests how agency is created (express vs. implied), how it is terminated, and the specific duties owed to principals versus third parties. It heavily features "dual agency" scenarios.

Instructor’s Study Tip: Focus on the timing of the Agency Disclosure Form (Disclosure, Election, Confirmation). The DRE loves to test on when these disclosures must happen in a transaction sequence.

Property Ownership and Land Use Controls (~15%)

What It Really Covers: This covers the different ways to hold title (Joint Tenancy, Community Property), encumbrances (liens, easements), and government powers (Zoning, Eminent Domain).

Instructor’s Study Tip: Understand the "Bundle of Rights." Many questions here are definition-heavy. If you know the difference between a specific lien and a general lien, you can pick up easy points here.

Property Valuation and Financial Analysis (~14%)

What It Really Covers: This is about appraisal theory (Cost, Income, and Market Data approaches) and economic principles of value (Substitution, Contribution).

Instructor’s Study Tip: Don't worry about complex math. The exam tests concepts, not calculations. Focus on knowing when to use the Income Approach (commercial/rentals) versus the Cost Approach (libraries/new schools).

Contracts (~12%)

What It Really Covers: This section deals with the validity of contracts (Competence, Mutual Consent, Lawful Object, Consideration) and the specific types of listings (Exclusive Right to Sell vs. Exclusive Agency).

Instructor’s Study Tip: Memorize the four essentials of a valid contract. Also, ensure you understand the "Safety Clause" in listing agreements—it’s a frequent exam target.

Financing (~9%)

What It Really Covers: This covers the primary vs. secondary mortgage markets, loan types (FHA, VA, Conventional), and consumer protection laws like TILA (Reg Z) and RESPA.

Instructor’s Study Tip: This is the smallest section for a reason. Do not spend weeks studying mortgage tables. Focus on the difference between the Trustor, Trustee, and Beneficiary in a Deed of Trust.

Transfer of Property (~8%)

What It Really Covers: This deals with deeds (Grant vs. Quitclaim), title insurance (CLTA vs. ALTA), and the escrow process.

Instructor’s Study Tip: This is often the easiest section to master because it is procedural. If you understand that a deed must be delivered and accepted to be valid (but not necessarily recorded), you are halfway there.

Salesperson vs. Broker Exam Content: What’s Different?

While both exams utilize the exact same seven categories, the lens through which you are tested changes.

The Salesperson exam focuses on the application of rules: "What form do I use?" or "What must I disclose?"

The Broker exam focuses on the above as well as a little more on supervision and management. In addition to the standard content, Broker candidates must understand:

Office management and supervision of salespersons.

Deeper liability regarding Trust Fund accounting.

More complex financial analysis and investment scenarios.

Is the content breakdown the same for salesperson and broker exams? Yes. The DRE uses the same "Content Outline" for both. However, the Broker exam contains 200 questions compared to the Salesperson's 150 and you have to score slightly better on the broker exam to pass.

For more on passing thresholds, read our breakdown of How the California Real Estate Exam is Scored.

How Content Weighting Should Shape Your Study Plan

Do not study every topic with equal intensity. The weighting reveals that the DRE values certain competencies over others.

High-Value vs. Low-Effort Topics

High-Value / High-Complexity: "Laws of Agency" and "Practice of Real Estate" combine for over 40% of your score. These require deep study because they are scenario-based. You cannot just memorize definitions; you must understand how to apply the law to a situation.

Low-Effort / Easy Points: "Transfer of Property" and "Property Ownership" often rely on static definitions (e.g., "What is a freehold estate?"). These are "low-effort" points. Master the vocabulary here to bank easy points, which gives you a buffer for the harder scenario questions.

Which exam topics give you the easiest points? Contracts and Transfer of Property. The rules in these sections are rigid and rarely change, making the questions straightforward if you know your definitions.

How the DRE Uses Weighting to Build and Score the Exam

The DRE uses a psychometric process called "equating" to ensure fairness. Whether you take the exam on a Tuesday in San Diego or a Friday in Oakland, the computer algorithm pulls questions to match this exact percentage blueprint.

Because the DRE uses this fixed blueprint, ADHI Schools’ practice exams mirror the real exam’s balance. When you take our mock tests, you are conditioning your brain to handle the exact distribution of topics you will face on test day.

How does knowing the content breakdown improve your odds on exam day?

It prevents panic. If you hit a hard run of Finance questions, you can relax knowing that Finance is only 9% of the exam. You can afford to miss a few hard finance questions and still easily pass if your Agency and Practice knowledge is solid.

To refine your testing tactics further, review our Multiple-Choice Strategy for the CA Real Estate Exam.

Mastering the blueprint gives you an immediate edge over other test-takers who are just memorizing flashcards without a plan.

Ready to start your structured preparation? Return to our California real estate exam guide to take the next step toward your license.

Frequently Asked Questions regarding DRE Exam Content

Do I need to pass each of the seven content areas individually?

No. Your score is cumulative. You do not need to score 70% in every single category to pass. For example, if you struggle with Financing (9%), you can make up for those missed points by scoring highly in Practice of Real Estate (25%) and Agency (17%).

Does the high weighting for Valuation and Financing mean there is a lot of math?

No. While Property Valuation (~14%) and Financing (~9%) make up nearly a quarter of the exam, the DRE focuses on concepts, not calculations. You will be tested on the principles of value and loan structures, but you will not be asked to perform complex arithmetic.

How strict are these percentages?

They are approximations provided by the DRE. On any given exam version, the specific number of questions may fluctuate slightly.

Is the "Practice of Real Estate" the hardest section because it is the largest?

Not necessarily. While it has the most questions (approx. 25%), many of them cover straightforward topics like Fair Housing and Truth-in-Advertising. Many students find the Laws of Agency section more difficult because it relies heavily on interpreting complex scenarios rather than memorizing facts.

|

You’ve passed your exam, you’ve hung your license with a broker, and you are ready to take over your local real estate market. You want to blast your face and name everywhere—billboards, Instagram, Read more...

You’ve passed your exam, you’ve hung your license with a broker, and you are ready to take over your local real estate market. You want to blast your face and name everywhere—billboards, Instagram, business cards, and flyers.

But before you order 5,000 glossy postcards, hit the brakes.

In my 20+ years of training agents, I’ve learned a hard truth: Most new agents don’t get in trouble for stealing money—they get in trouble because they violated DRE rules in their marketing and they might not have even known it.

You do not want your first letter from the Department of Real Estate to be an accusation. The DRE does audit websites, postcards, and social profiles—especially when a complaint comes in—so assume your advertising will be reviewed at some point.

The DRE is incredibly strict about how licensees present themselves. If you don’t follow the specific DRE advertising rules, you aren't just looking at a warning; you could be facing citations, fines, and a permanent mark on your record.

Here is your plain-English guide to marketing yourself aggressively without getting flagged.

The "First Point of Contact" Rule

The most fundamental concept in California real estate advertising is the "First Point of Contact."

This is the moment a consumer first encounters you professionally. Because the public relies on these materials to verify your identity, the DRE mandates strict transparency here. Think of your license status as the very first disclosure you make to a client. (For more on what you must reveal later in the transaction, see our California Disclosure Laws (Complete Breakdown)).

What Counts as "First Point of Contact" Materials?

The DRE defines this broadly. If you use it to get business, it counts. In the regulations, these are called "solicitation materials"—anything you use to solicit business from the public. These include:

Business cards

Stationery and letterhead

Email signatures

Flyers, door hangers, and mailers

"For Sale" and open house signs

Website homepages and landing pages

Online lead forms and "contact me" pages

The Mandatory Trio

For any of the materials listed above, you must include three specific items:

Your Name: Exactly as it appears on your license (no nicknames unless filed as a "DBA").

Your License Identification Number: This is non-negotiable.

Your Responsible Broker’s Identity: You cannot advertise as a "lone wolf." The public must know which brokerage employs you.

Digital & Social Media Compliance

The internet moves fast, but the law keeps up. Under Commissioner's Regulation 2770, electronic and online advertising is treated just like traditional solicitation—your license status must still be clear.

Here is how to stay compliant on different platforms:

Social Media Bios (Instagram, TikTok, Facebook)

Your bio is your digital business card. It must include:

Your name.

Your DRE license number.

Your responsible broker’s identity.

Warning: Do not bury this information deep inside a Linktree. If a consumer clicks your link, and then has to click again to find your license info, you are technically "two clicks" away. That is a violation. Put the DRE# directly in your bio text.

Individual Posts, Reels, and Stories

Does your license number need to be in the caption of every single Instagram story or Tweet? Generally, no—provided you follow the "One-Click Rule."

You are compliant if your individual posts clearly relate back to a main profile (your bio) where the mandatory information is displayed. As long as the consumer can find your license status with one single click from the post, you are safe.

Websites, Landing Pages, and Lead Forms

Websites are different. You cannot rely on the "one-click" rule here. Your license number and broker identity should appear on the homepage or, ideally, globally in the footer of every page. If a consumer lands on a blog post or a listing page, they should not have to hunt to see who you are.

"Team Name" Advertising Pitfalls

This is where I see the most citations for established agents. Everyone wants a flashy team name like "The Luxury Living Group," but the DRE sees "Teams" as a potential source of consumer confusion.

If you follow these real estate team advertising rules California sets out, your signs and online branding will stay out of trouble:

1. The Surname Rule

A team name must include the surname (last name) of at least one licensee on the team.

Illegal: "The Magic City Team"

Legal: "The Smith Group."

2. The Permitted Words

Your team name must include a term like "Group," "Team," or "Associates." You cannot use words that imply you are a standalone brokerage, such as "Real Estate," "Brokerage," or "Company."

3. The Font Size Rule (The "Ego Check")

This is a technicality that leads to fines. When you advertise a team name, the Responsible Broker’s identity must be displayed as prominently as the team name.

This ties directly to agency relationships. As we explain in California Agency Law Explained for New Agents, you represent the broker, and the broker represents the client. Your ads must reflect that legal hierarchy.

Discriminatory Advertising

Advertising rules aren't just about font sizes; they are about civil rights. When writing listing copy, you must avoid language that suggests a preference or limitation based on a protected class.

In California, that includes: race, color, religion, sex, gender, gender identity, sexual orientation, marital status, national origin, ancestry, familial status, disability, and source of income.

Bad: "Perfect bachelor pad" (implies sex/familial status preference).

Bad: "Walking distance to synagogue" (implies religious preference).

Good: "Great starter home" or "Close to places of worship."

For a full list of words that can trouble you, read our guide: California Fair Housing Laws Agents Must Know.

Misleading Advertising & "Blind Ads"

Honesty is the baseline. Under the Business and Professions Code, making any substantial misrepresentation is grounds for license suspension.

Puffery vs. Fraud

"Puffery" is an opinion that isn't expected to be taken as literal fact (e.g., "The most beautiful view in the city!").

This is allowed.

Fraud is retouching a photo to remove power lines or claiming a home is 3,000 sq. ft. when tax records say 2,200.

False Authority & Inventory Tricks (Don't Do This)

The "Top Producer" Trap: Do not call yourself the "#1 Agent in the City" unless you have verifiable data to prove it for that specific timeframe.

The "Just Sold" Trick: Do not advertise a property as "Just Sold" if you were not the listing or selling agent, unless you explicitly credit the actual agent.

The "Specialist" Claim: Be careful claiming you are a "Probate Specialist" or "REO Expert" if you have no certification or track record in those niches.

Blind Ads

A Blind Ad is any advertisement that hides the fact that you are a licensed real estate agent or fails to identify your broker.

Bad: "I buy homes for cash, call 555-0199" with no name, license status, or broker.

Good: "Fred Smith, XYZ Real Estate, Licensed Real Estate Broker (DRE# 09944), buys homes for cash. Call 555-0199."

Just like commingling is the top financial violation, improper advertising is the top administrative violation. (See: What Is “Commingling” in California Real Estate?).

Safe Advertising Checklist (2026 Edition)

Before you hit "publish" or "print," run your materials through this checklist.

Business Cards

Name (as licensed)

California real estate license number on business cards (labeled "DRE#" or "Lic#")

Responsible Broker’s Name/Logo

Email Signature

Full Name

DRE License #

Broker Name (must be present in every email sent to clients)

Social Media Bio

Name

DRE License # (Directly in text, not hidden in a link)

Broker Affiliation

Postcards & Flyers

Does the sign identify the broker?

If a team name is used, does it have a surname or valid DBA?

Font Check: Is the broker's name equal to or larger than the team name?

Online Ads (Google/Facebook)

Is your license number and brokerage affiliation in the ad?

Website / Landing Pages

DRE License # appears on the homepage or in a global footer visible from every page.

Broker’s name/logo appears in the header or footer.

Lead forms make it clear you are a licensed real estate agent.

Next Step: Lock In Your Compliance Knowledge

Advertising is just one piece of your legal footprint. Your license is your livelihood—don’t risk it for a cute slogan or minimalist design.

For a complete breakdown of the rules that govern your career—from trust funds to agency disclosures—bookmark and study our California Real Estate Laws & Compliance Guide. That is your roadmap to staying safe, compliant, and in business for the long term.

Frequently Asked Questions

Q: What must be included on a California real estate business card?

A: Under DRE "First Point of Contact" rules, your business card must include three mandatory items: your name exactly as it appears on your license, your DRE license identification number, and the identity of your responsible broker. Omitting the broker’s name is a common violation.

Q: Do I need to put my DRE license number on every Instagram post or Story?

A: Generally, no. Under the "One-Click Rule" (Commissioner's Regulation 2770), you do not need your license number on every individual post if that post links directly to a profile (like your Bio) where your name, license number, and broker affiliation are clearly displayed.

Q: Can I put my real estate license number in my Linktree or bio link?

A: No, this is risky. The DRE requires your license status to be accessible within "one click." If a consumer clicks your bio link and then has to click again inside a menu (like Linktree) to find your license number, you are technically two clicks away, which can be considered a violation. Place your DRE# directly in your Instagram or TikTok bio text.

Q: What are the rules for real estate team names in California?

A: A team name must include the surname (last name) of at least one licensee on the team and a term like "Group," "Team," or "Associates." You cannot use terms that imply you are a separate brokerage, such as "Real Estate," "Company," or "Corp."

Q: Does my broker’s name have to be the same size as my team name on signs?

A: Yes. The DRE requires that the responsible broker’s identity be displayed as prominently as the team name. If your team name is in a large font, your broker’s name cannot be a tiny footnote; it must be reasonably equivalent in size to prevent consumer confusion.

Q: What is a "blind ad" in real estate?

A: A blind ad is any solicitation material that fails to identify the advertiser as a licensed real estate agent or fails to identify their responsible broker. For example, a Craigslist ad saying "I buy homes for cash" without a license number or broker name is a prohibited blind ad.

|

The California Department of Real Estate (DRE) salesperson exam is notorious for its 50% fail rate, but that number is misleading. It’s not an impossible test; it’s just a specific one. Most students Read more...

The California Department of Real Estate (DRE) salesperson exam is notorious for its 50% fail rate, but that number is misleading. It’s not an impossible test; it’s just a specific one. Most students fail because they study the wrong things. Here is the good news: the DRE tells us exactly what matters. Master these core areas, and you remove the mystery—and the risk—from exam day.

If you haven’t already reviewed our comprehensive California real estate exam guide, start there for an overview of the full licensing journey.

The 7 Major Content Areas (DRE Syllabus)

The DRE structures the real estate license syllabus into seven competency areas. Each represents a skill set you must demonstrate to pass the DRE salesperson exam. Below is a clear breakdown of what you’re expected to know in each and this is true regardless of the sales or broker exams. Sure, the number of questions on each exam is different, but the topics are the same across both tests.

Practice of Real Estate and Mandated Disclosures

This is the heart of the DRE exam and the section where students commonly underestimate the depth of material. Expect scenario-based questions that test whether you can apply real estate principles, ethical rules, and disclosure laws correctly.

Key concepts include:

Trust Fund Handling: Proper receipt, deposit, reconciliation, recordkeeping, and the consequences of commingling or conversion.

Fair Housing Laws: Federal and California anti-discrimination statutes, protected classes, blockbusting, steering, and reasonable accommodation requirements.

Transfer Disclosure Statements: What must be disclosed, who must sign, defects that trigger disclosure, and exemptions.

Ethics & Prohibited Conduct: Unlawful misrepresentation, duties of honesty and fair dealing, advertising rules, and handling offers.

Laws of Agency and Fiduciary Duties

You’ll be tested on how agency relationships are created, how they are terminated, and what fiduciary duties a licensee owes.

Key concepts include:

Agency Disclosure Timing: When and how the Agency Disclosure form must be delivered, acknowledged, and confirmed in a transaction.

Creation of agency: express, implied, ostensible, ratification.

Disclosure obligations in agency relationships.

Fiduciary duties — loyalty vs. honesty and fairness to all parties.

Dual agency rules and the unique risks and requirements involved.

Consequences of breaching fiduciary duties and permitted vs. prohibited conduct.

Property Ownership and Land Use Controls

This section examines the legal framework that governs how property is held, controlled, and regulated in California.

Key concepts include:

Types of ownership: joint tenancy, tenancy in common, community property.

Land use controls: zoning, variances, conditional use permits.

Government powers: police power, eminent domain, taxation, escheat.

Public and private restrictions (CC&Rs, HOA rules).

Legal property descriptions and boundaries.

Property Valuation and Financial Analysis

You don’t need to be an appraiser, but you do need a solid grasp of how value is estimated and how income-producing properties are analyzed.

Key concepts include:

Three approaches to value: market, cost, and income.

Appraisal fundamentals: substitution, conformity, contribution, and regression.

Income concepts: gross rent multiplier (GRM), net operating income (NOI), and capitalization basics.

What affects property value: supply and demand, neighborhood cycles, economic forces.

Understanding when each valuation approach is appropriate.

Contracts

Contracts appear all over the exam because they appear all over real estate practice.

Key concepts include:

Essential elements of a valid contract (capacity, mutual consent, lawful object, consideration).

Listing agreements: exclusive right to sell, exclusive agency, open listings.

Residential purchase agreements and common contingencies.

Offer and acceptance rules, counteroffers, termination.

Enforceability and consequences of breach.

Financing

Expect questions that test your understanding of lending systems and consumer protection laws.

Key concepts include:

Primary vs. secondary mortgage markets.

Loan products: conventional, FHA, VA, adjustable-rate, and seller financing.

TILA/RESPA integration (TRID) requirements and timing.

Points, loan origination, and discount points.

Mortgage defaults, foreclosure basics, and rights of reinstatement or redemption.

Transfer of Property

This section deals with how real estate actually changes hands — legally and procedurally.

Key concepts include:

Deeds: grant, quitclaim, warranty, essential elements, delivery.

Title insurance: CLTA vs. ALTA, exclusions, and protections.

Escrow process: prorations, instructions, trustworthiness requirements.

Recording and priority rules.

Property taxes, assessments, and transfer fees.

Is the Exam Content the Same Every Year?

The core real estate principles remain remarkably stable year to year, but the DRE updates exam questions periodically to reflect changes in law, disclosures, lending rules, and fair housing standards. For a deeper breakdown of how topics evolve, review our current California Real Estate Exam content breakdown.

How Deeply Do You Need to Know These Topics?

Whether you are taking the sales license or broker exam, passing is not about memorizing isolated facts — it tests whether you can apply concepts to realistic scenarios. The better you understand the underlying real estate principles, the easier it becomes to eliminate wrong answers. To fully prepare, you should also understand how the real estate exam is scored and exactly how many questions are on the exam so you can manage your time effectively.

Strategy for Mastering the Material

Focus on understanding, not cramming. Most students waste time over-studying math (there isn’t any math on the exam) or memorizing obscure details. Instead:

Study in short, focused bursts.

Use process-of-elimination on questions with similar answer choices.

Prioritize practice questions that mirror DRE logic.

Review mistakes deliberately — they reveal pattern gaps.

To sharpen your testing approach, study our multiple-choice strategies, which are specifically designed for the DRE salesperson exam.

Mastering the seven core areas of the real estate license syllabus is the most reliable path to passing the California Department of Real Estate exam. With the right preparation, consistent practice, and a clear understanding of what the DRE is looking for, you’ll walk into the testing center confident and ready.

Begin your focused review today — the exam is challenging, but absolutely conquerable with the right strategy and guidance.

FAQ: What’s on the California Real Estate Exam?

Is the California real estate exam hard?

It’s challenging, but not because the material is impossible. The exam is hard for people who study the wrong things. If you understand the seven DRE content areas and practice scenario-based questions, it becomes very manageable.

How many questions are on the California real estate exam?

The salesperson exam has 150 questions and the broker exam has 200 questions. Both are multiple-choice and both are timed.

How long do you get to finish the exam?

Salesperson: 3 hours and 15 minutes

Broker: 4 hours

There are no scheduled breaks, so pacing matters.

Does the exam include math?

No. The DRE removed math years ago. You may see questions about valuation concepts (like cap rates or GRM), but you won’t be asked to calculate formulas.

What score do you need to pass?

Salesperson: 70%

Broker: 75%

The DRE does not curve scores and does not release which questions you missed.

Is every exam the same?

No. There are multiple versions in circulation, and the DRE updates questions periodically. However, the content areas and competency weights stay consistent year to year.

Does the DRE test more scenarios or definitions?

Scenarios dominate. Many questions test whether you can apply a rule—not just recognize a definition. This is especially true in agency, disclosures, ethics, and trust fund handling.

Which section of the exam is the hardest?

Most students struggle with:

Practice of Real Estate & Disclosures

Agency & Fiduciary DutiesThese are heavily scenario-based and require understanding, not memorization.

Can you bring notes, calculators, or reference materials?

No. The exam is closed-book, and the testing center provides everything you’re allowed to use.

Are the salesperson and broker exams based on the same topics?

Yes. The subject areas are the same, but the broker exam goes deeper and includes more questions per topic.

How often can you retake the exam?

As many times as needed. There is no waiting period. The only requirement is paying the re-exam fee and scheduling a new appointment.

What’s the best way to prepare for the content areas?

Use practice questions that mirror DRE logic, focus on the most heavily weighted topics, and study in short, consistent sessions. Understanding beats cramming.

Are exam questions pulled from a public question bank?

No. The DRE does not publish exam questions. Any company claiming to have “real exam questions” is misleading you.

What topics should I NOT waste time studying?

Detailed math

Obscure federal laws that rarely appear

Commercial-only concepts not tied to the syllabus

Hyper-technical appraisal jargon

The DRE sticks closely to the seven official content areas.

Does the exam focus on California-specific laws?

Yes. Proper disclosures, agency rules, trust fund handling, and fair housing compliance are all tested from a California perspective, not a national one.

|

Disclaimer: This guide is intended for educational purposes only and should not be taken as legal advice or used as a substitute for professional counsel. While every effort has been made to Read more...

Disclaimer: This guide is intended for educational purposes only and should not be taken as legal advice or used as a substitute for professional counsel. While every effort has been made to ensure accuracy, fair housing laws and DRE regulations are subject to change. Please consult a licensed attorney or your broker regarding specific compliance scenarios.

In real estate, we often worry about low appraisals, difficult inspections, or financing falling through.

But fair housing is another place where careers go sideways. You can price a home perfectly and negotiate like a shark, but if you mishandle a protected class issue, you aren't just looking at a lost commission; you're looking at DRE discipline, federal lawsuits, and a destroyed reputation.

This isn't just about memorizing a list of laws for your exam. This is a survival manual for California agents who want to stay compliant, stay ethical, and stay in business.

What Is Fair Housing? (The "Plain English" Version)

Simply put, fair housing means everyone gets a fair shot at a home, no matter where they come from or what they look like. It's a simple idea that can get complicated in real-world application.

It is illegal to discriminate in the sale, rental, or financing of housing. This includes refusing to rent or sell, setting different terms or conditions, or advertising any preference or limitation based on protected characteristics.

While the Federal Fair Housing Act of 1968 set the baseline (protecting race, religion, sex, etc.), California took those rules and expanded them. Historically, California led with the Rumford Fair Housing Act, but today we operate primarily under the Fair Employment and Housing Act (FEHA) and the Unruh Civil Rights Act.

Note: While federal statutes don't explicitly list "Sexual Orientation" or "Gender Identity," HUD currently enforces the Fair Housing Act to protect these classes. California law, however, explicitly codifies them.

The Golden Rule: Never assume that complying with the basic federal list is enough. California’s protections are broader, covering everything from marital status to source of income.

Protected Classes

If you memorize only the federal list, you might be leaving yourself exposed in California. Here is the breakdown of who is protected.

Federal Protected Classes

Race

Color

Religion

Sex (includes sexual orientation and gender identity per HUD enforcement)

National Origin

Familial Status (families with children under 18, pregnant persons, and those securing child custody)

Disability (mental and physical)

California Additional Protections (FEHA) In California, the Fair Employment and Housing Act (FEHA) explicitly adds:

Source of Income (Crucial for Section 8/Voucher holders)

Sexual Orientation (Explicitly stated in CA statute)

Gender Identity and Gender Expression

Marital Status

Military or Veteran Status

Ancestry

Genetic Information

Protections Under the Unruh Civil Rights Act In addition to FEHA, California’s Unruh Civil Rights Act prohibits discrimination in all business establishments (including housing) based on arbitrary characteristics. This covers:

Age

Medical Condition

Citizenship / Immigration Status

Primary Language

Arbitrary Discrimination

The takeaway: If a client asks you to filter buyers or tenants based on who they are rather than financial qualification, your internal alarm bells should be ringing.

Common Ways Agents Get in Trouble (Real-World Scenarios)

In my classes, I often hear agents say, "I would never discriminate!" But discrimination is rarely a mustache-twirling villain slamming a door. It’s usually subtle, accidental, or done with "good intentions."

Here are some common traps agents fall into.

1. The "Perfect Neighborhood" Trap (Steering)

The Scenario: A buyer asks, "I have young kids. Which of these neighborhoods is the best fit for a family like mine?"

The Mistake: The agent replies, "Oh, you want the north side. The south side is mostly singles and retirees, you wouldn't be comfortable there."

Why It’s Illegal: This is steering. It is illegal to direct a client toward or away from a neighborhood based on familial status or age composition.

The Fix: Stick to objective criteria. Suggested response: "I can’t steer you based on demographics, but I can show you homes near the specific schools, parks, or amenities you’re interested in."

2. The "No Vouchers" Landlord (Source of Income)

The Scenario: You are the listing agent for a rental. The landlord tells you, "I don’t want to deal with Section 8 paperwork. Just put 'No Section 8' in the private remarks."

The Mistake: You follow instructions.

Why It’s Illegal: In California, "source of income" is a protected class. Denying a tenant solely because they use a housing subsidy is illegal.

The Fix: View the voucher as a valid income source. Under California law (SB 267/SB 329), when calculating rent-to-income ratios (e.g., 3x rent), it must be based only on the tenant’s portion of the rent, not the total rent amount. Using the full rent amount to disqualify a voucher holder is discriminatory.

3. The "Ideal Buyer" Ad (Discriminatory Advertising)

The Scenario: You’re listing a cute 1-bedroom condo near a university. You write: "Perfect bachelor pad!" or "Great for active young professionals!"

The Mistake: You described the person, not the property.

Why It’s Illegal: This implies a preference for single people or younger people, potentially discriminating against families or older adults.

The Fix: Focus on the features. "Cozy 1-bedroom with low maintenance yard and close proximity to nightlife." For a deeper dive on what you can and cannot say in marketing, review our guide on Advertising Laws for California Real Estate Agents.

How to Handle Discriminatory Client Requests (Scripts)

This is the hardest part for new agents. You want to please your client, but you cannot break the law. When a client asks you to discriminate, you need a script ready so you don’t freeze.

Scenario A: The Seller who wants to pick "Neighbors like us"

Client says: "I want to make sure the buyer is a 'good fit' for this Christian community."

Your Script: "I understand you care about the neighborhood, but as a real estate professional, I am legally required to show your home to all qualified buyers regardless of their religion. Restricting the sale based on religion would violate fair housing laws and put both of us at risk. We need to focus on the best offer with the strongest financial terms."

Scenario B: The Landlord refusing Section 8

Client says: "I'm not doing the voucher thing. Just tell them the place is rented."

Your Script: "I cannot do that. In California, refusing a tenant based on their source of income—including vouchers—is illegal. If they meet your credit score requirement and income threshold, we have to process their application just like anyone else’s. Disqualifying them for a voucher could lead to a significant fine for you."

Scenario C: The Buyer asking about crime/race

Client says: "Is this a 'safe' area? What kind of people live here?"

Your Script: "I can’t discuss demographics, as that violates fair housing guidelines. However, I can direct you to the local police department’s website for crime statistics so you can make an informed decision based on the data."

You have a fiduciary duty to your client, but that duty never extends to breaking the law. For more on navigating these duties, read how California Agency Law Explained for New Agents outlines your responsibilities.

Fair Housing in Advertising: Do’s and Don’ts

Your MLS remarks and social media captions are permanent records. If you use discriminatory language, you are creating evidence against yourself.

The Golden Rule of Ad Copy: Describe the property, not the person.

DON'T Use: "Perfect for families," "Bachelor pad," "No kids," "Able-bodied only," "Empty nesters' dream."

DO Use: "Large backyard," "Near places of worship," "Studio apartment," "Second-floor walk-up," "Quiet neighborhood."

Advertising is one of the easiest ways to get flagged. For an intro to this topic, check out our California Real Estate Laws & Compliance Guide before hitting publish.

Reasonable Accommodations & Assistance Animals

Many landlords (and agents) get confused here.

Reasonable Accommodation: A change in rules or policies. (e.g., Waiving a "guest parking only" rule for a caregiver).

Reasonable Modification: A physical change to the property (e.g., Installing a ramp). In most rentals, the tenant pays for this, but the landlord must allow it.

The "No Pets" Policy vs. Assistance Animals Service animals and support animals are not pets. You cannot charge a "pet deposit" or "pet rent" for them, and you cannot enforce a "no pets" policy against them.

The Financial Rule: While you cannot charge a fee upfront, the tenant is still financially liable for any actual damage the animal causes to the property.

Denial: You can only deny the request if it poses an undue financial/administrative burden or a direct threat to health/safety—a very high bar to prove.

Risk Management & Compliance Checklist

Before you take a listing or sign a lease, run through this mental checklist

Initial Client Briefing: Have you explained to the seller/landlord that you adhere strictly to fair housing laws? (Do this before they ask you to discriminate).

Ad Review: Have you removed all references to prohibited demographics in your marketing?

Uniform Screening: Are you asking every applicant the exact same questions? Inconsistency is the breeding ground for discrimination claims.

Documentation: If you reject an offer or application, do you have a written, legal reason why (e.g., credit score, income ratio, lower price)?

Disclosure: Are you being transparent? Transparency prevents lawsuits. Check our California Disclosure Laws (Complete Breakdown) to ensure you aren't hiding facts that could look like discrimination later.

Enforcement: The Reality Check

Who watches this? The California Civil Rights Department (CRD) and federal HUD investigators.

If a complaint is filed against you:

Investigation: It is invasive, stressful, and time-consuming.

Penalties: You could face actual damages (money to the victim), civil penalties (fines to the government), and attorney’s fees.

License Discipline: The DRE can suspend or revoke your license.

Ignorance is not a defense. Saying you didn’t know source of income was protected won’t work. Fair housing violations are treated as seriously as mishandling trust funds. Just as you need to understand What Is "Commingling" in California Real Estate?, you must understand fair housing to keep your license safe.

Final Thoughts

Fair housing law can feel complex, but if you build the right habits—focusing on objective criteria, using the right scripts, and treating every person with the same professional standard—it becomes second nature.

Don't treat this as just "compliance homework." Treat fair housing as a core skill of being a top-tier agent. It protects your community, and it protects your career.

Need to brush up on other critical regulations? Head over to our California Real Estate Laws & Compliance Guide for the full breakdown.

Fair Housing FAQs: The Survival Guide

Q: Is following the Federal Fair Housing Act enough to keep me safe in California?

A: No. California took federal laws and "supersized" them. While federal law covers the basics (race, religion, sex), California adds strict protections for Source of Income, Marital Status, and Immigration Status. If you only memorize the federal list, you are leaving yourself exposed to liability.

Q: My landlord doesn’t want to accept Section 8 vouchers. Can I put "No Section 8" in the remarks?

A: Absolutely not. In California, "Source of Income" is a protected class. You cannot deny a tenant solely because they use a housing subsidy. Furthermore, you cannot disqualify them because they don't make 3x the total rent. You must calculate their income threshold based on the tenant’s portion of the rent.

Q: A buyer asked for a "safe" neighborhood with "families like ours." Can I steer them to the right area?

A: You cannot. "I cannot provide personal opinions on 'safety' or demographics, as subjective comments can be interpreted as 'steering,' which violates fair housing laws. However, I can direct you to the local police department’s website for objective crime statistics so you can make an informed decision based on data."

Q: Can I market a small condo as a "Perfect Bachelor Pad"?

A: No. That implies a preference for single men and discriminates against families or women.

The Golden Rule of Ad Copy: Describe the property (e.g., "cozy 1-bedroom," "near nightlife"); not the person you think should live there.

Q: Can a landlord charge a pet deposit for a service animal?

A: Never. Service and support animals are not pets—they are accommodations for a disability. You cannot charge pet rent or deposits, and "No Pet" policies do not apply to them.

|

In the high-stakes world of California real estate disclosure laws, lawsuits rarely happen because a house was sold for $5,000 less than asking. They happen because the garage floods every January, the Read more...

In the high-stakes world of California real estate disclosure laws, lawsuits rarely happen because a house was sold for $5,000 less than asking. They happen because the garage floods every January, the seller knew about it, and nobody told the buyer.

For most new agents, the first serious risk of a lawsuit or DRE complaint comes from inaccurate and incomplete disclosures—not from writing a weak offer.

You might be terrified of missing a checkbox, "forgetting" a document, or getting dragged into court because your seller hid an active leak behind a fresh coat of paint. I’ve been teaching real estate for over 20 years at ADHI Schools, and I’m also a practicing broker who has watched real disclosure disputes play out in the real world

I tell my students constantly: Disclosures aren’t busywork. They are your shield.

When done correctly, they protect your client, your paycheck, and your license. This guide is a practical, street-level breakdown of real estate disclosure requirements in California, the forms you must master, and the scripts you need to stay out of trouble.

(Disclaimer: This article is for educational purposes only. If you are facing a specific legal situation or complex transaction, always consult your managing broker or a qualified real estate attorney.)

What Are “Disclosures” in California Real Estate?

In plain English, a disclosure is the formal act of revealing material facts about a property.

California is a strict "consumer protection" state. Unlike "Caveat Emptor" (Buyer Beware) states where the buyer is on their own, California places a heavy burden on the seller and the agents to reveal what they know.

The "Material Fact" Standard

A material fact is any information that would affect the value or desirability of the property to a reasonable person.

Does the roof leak? Material fact.

Was the garage converted without a permit Material fact.

Is there a noisy firing range a mile away? Likely a material fact.

The "Loud Party" Rule (A Real-World Example)

To understand "desirability," consider this scenario: I once saw a deal where the seller didn’t mention a neighbor who hosted loud backyard parties every single weekend. The buyer called the listing agent at 11:30 p.m. on their first Saturday in the home, furious.

Was the house physically broken? No. Was the desirability affected? Absolutely. If you find yourself wondering, "Should we mention this?" the answer is almost always yes.

The Core California Real Estate Disclosure Laws Framework (The Big 6 Forms)

While there are dozens of forms, these are the heavy hitters that form the backbone of California disclosure rules.

1. The Transfer Disclosure Statement (TDS)

The TDS is the holy grail. It is a statutory form where the seller must list items included in the sale, whether they work, and any significant defects (walls, fences, electrical, plumbing).

Crucial Rule: The seller must fill this out—not the agent. You can explain the form, but never put the pen to paper for them.

2. Seller Property Questionnaire (SPQ)

While the TDS is law, the SPQ is a standard C.A.R. form used by most brokerages to expand on the disclosures in the TDS. It asks pointed questions about deaths on the property, insurance claims, pets, and neighborhood nuisances, among others.

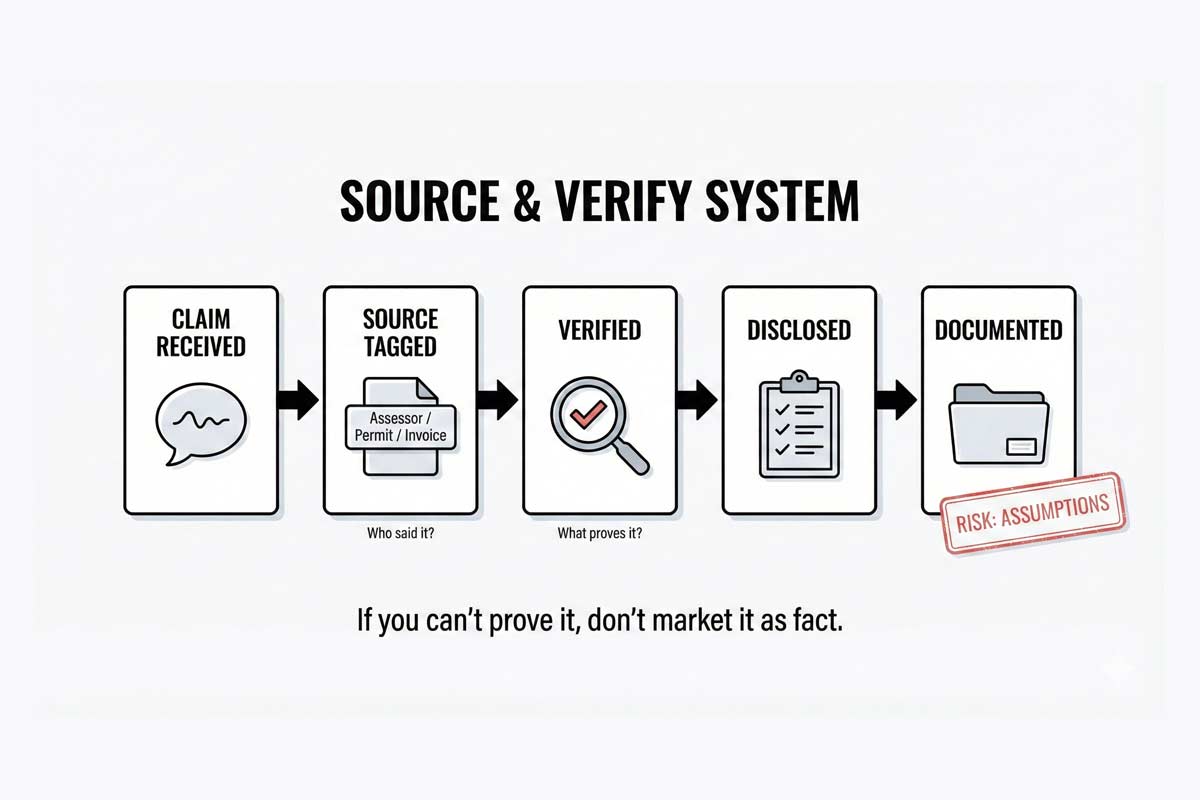

3. Agent Visual Inspection Disclosure (AVID)

This is your duty. California Civil Code requires real estate agents to conduct a "reasonably competent and diligent visual inspection" of accessible areas.

What to write: Observations. "Stain on ceiling in bedroom 2," "Cracked tile in entryway."

What NOT to write: Diagnoses. Do not write "Roof was leaking, but no longer active." You are not a roofer.

4. Natural Hazard Disclosure (NHD) Statement

California is beautiful but high-risk from a natural hazard standpoint. The NHD report tells the buyer if the home sits in flood, fire, or earthquake zones.

Pro Tip: Most agents order this from third-party companies to reduce liability. However, a third-party report doesn't erase your duty. You still must read the report and flag major issues for your client.

5. Condo/HOA Disclosures

If you are selling a condo or a home in an HOA, the standard forms aren't enough. You must provide the CC&Rs, bylaws, financial statements, and meeting minutes.

Why it matters: Many disputes arise because a buyer didn't know about a "special assessment" coming down the pipe or a rule banning their pickup truck from the driveway.

6. Lead-Based Paint Disclosure

If the home was built prior to 1978, federal and state law requires this disclosure and the provision of the "Protect Your Family from Lead in Your Home" pamphlet.

Deep Dive: To see how these forms fit into the bigger legal picture, check out our California Real Estate Laws & Compliance Guide.

Who Must Disclose What? (And What to Say)

A common source of confusion is figuring out who is "on the hook" for specific information.

The Seller's Duty (and the "Investor" Myth)

The seller must disclose known material facts. They don't have to hire inspectors to find new defects, but they cannot hide what they know, or should know.

The "I Never Lived There" Trap: Many investors, flippers, or heirs selling a probate property believe they are exempt from disclosures because they "never lived there." This is false. While they may be exempt from the TDS in specific cases (like a trustee selling a property at a trustee sale foreclosure auction), they are generally not exempt from disclosing known material facts. "I never lived there" is not a magic shield against known material facts.

The "Flipper" Law (AB 968): The End of "I Don't Know" For years, investors used the "I never lived there" excuse to avoid disclosing property defects. As of July 1, 2024, that loophole is gone for flippers.

Under Assembly Bill 968, if you are selling a single-family home (1-4 units) within 18 months of buying it, you have a heightened duty. You cannot just hand over a blank TDS. You must legally disclose:

The Work Done: A written list of every renovation, modification, or repair.

The Contractors: The names and contact info for the contractors who did the work.

The Permits: Copies of the permits. If you don't have them, you must provide the contact info for the third party who does.

The trap: If you hired cheap, unlicensed labor to paint over a problem and didn't pull permits, you now have to hand that evidence directly to the buyer. If you fail to do this, you aren't just risking a lawsuit; you are handing the buyer a roadmap to win it.

The Listing Agent's Duty

You have a duty of honest dealing and a duty to inspect. You cannot hide behind your seller.

The "Don't Tell Them" Script: If a seller says, "The roof leaks, but don't tell the buyer," and you obey, you can get yourself in hot water. Here is the script to handle that:

"Mr. Seller, I am required by law and by my real estate license to disclose this. If we hide it, we open ourselves up to a lawsuit we will have a tough time defending against."

The Buyer's Agent's Duty

You must review disclosures with your buyer and point out red flags.

The "CYA" Email Script: Don't just verbally tell a buyer to get an inspection. Document it.

"Hi [Buyer Name], per our conversation, I strongly recommend we hire a licensed specialist to inspect the roof before your contingency period ends on Tuesday. The general inspection noted wear, and I want to ensure you know the full scope."

This email could save you one day. For a deeper dive into your fiduciary duties and how they relate to disclosures, read California Agency Law Explained for New Agents.

Timing, Delivery & Documentation

It’s not enough to fill out the forms; you have to deliver them correctly.

The Timeline

In a standard California Residential Purchase Agreement (RPA), the seller typically has 7 days after acceptance to deliver full disclosures, unless otherwise agreed in writing.

Handling Prior Reports

If a previous escrow fell out and the buyer left you with their inspection report, can you ignore it?

No.

If you or the seller have a report in your possession, it is now part of what you know about the property. Talk to your broker about office policy, but in most cases you should provide it to the new buyer.

Script: "Please find the attached inspection report from a previous transaction, provided for informational purposes only. We recommend you conduct your own investigations."

High-Risk Topics Agents Must Never Gloss Over

In my experience, these are the landmines that cause the most explosions:

1. Water Intrusion & Mold

Never let a seller paint over a water stain without disclosing the cause.

2. Unpermitted Work

Did they turn the garage into a gym? Disclose it.

3. Death on the Property

You must disclose death on the property within the last 3 years. If a buyer asks directly about death anytime in the past, you must answer honestly.

4. Neighborhood Nuisances

Noises, odors, or disputes that affect "desirability."

The "Compliance Stack": How It All Connects

California real estate disclosure laws are just one layer of your compliance defense. Think of your "Compliance Stack" like this:

Disclosures: What you tell the buyer about the house.

Agency: Who you represent and your fiduciary duties.

Fair Housing: What you never say (avoiding discrimination).

Read more: California Fair Housing Laws Agents Must Know

Advertising: What you put in print/online (avoiding false claims).

Read more: Advertising Laws for California Real Estate Agents

Trust Funds: How you handle the money (avoiding commingling).

Read more: What Is “Commingling” in California Real Estate?

Most serious lawsuits involve a failure in two or three of these layers at once.

The Cost of Silence: What Happens If You Fail to Disclose?

If you fail to follow seller disclosure laws in California, the consequences are severe:

Rescission: The deal unwinds.

Damages: You pay for the difference in value and repairs.

DRE Discipline: You have suspension or revocation of your license.

Practical Checklists & Scripts

To protect yourself, use these tools in every transaction.

The "Mental Stop" Checklist

Before you send a packet, ask:

Did the seller answer every question on the TDS/SPQ? (No blanks).

Did I walk the property and write down exactly what I saw on the AVID?

Did we disclose any unpermitted work we are aware of?

Are we sitting on any old inspection reports that need to be shared?

Script: Explaining the AVID to a Buyer

"I’ve completed my Agent Visual Inspection Disclosure. Please keep in mind, I am a real estate agent, not a contractor. I’m noting what I see—like a stain or a crack—but I cannot tell you if it’s structural or cosmetic. That is why we need a professional home inspection."

Frequently Asked Questions About California Disclosure Laws

Do seller disclosure laws in California apply to “as-is” sales?

Yes. “As-is” usually means the seller doesn’t plan to make repairs, but they still must disclose known material defects.

Do I have to disclose a death on the property in California?

Yes, if it occurred within the last three years. If a buyer asks directly about any past death, you must answer honestly.

Are investors exempt from real estate disclosure requirements in California?

No. Even if they never lived in the property, they must disclose any material facts they know.

Can I rely only on the NHD company and inspector reports?

No. They help reduce risk, but you’re still expected to read them and flag major issues for your client.

Understanding California disclosure laws is about more than just passing your exam. It’s about building a career that lasts. When you master these forms, you aren't just pushing paper—you are establishing yourself as a pro who knows how to navigate risk.

If you’re not licensed yet and this article made you realize how serious this business is, that’s a good thing.

Read our California Real Estate Laws & Compliance Guide to see the big picture, or explore our classes to get the kind of training that actually prepares you for the real world.

|

Agency Is Where Agents Get Sued

If you ask a seasoned real estate attorney where most lawsuits begin, they won’t tell you that it’s always about a leaky roof or a cracked slab. They will tell you Read more...

Agency Is Where Agents Get Sued

If you ask a seasoned real estate attorney where most lawsuits begin, they won’t tell you that it’s always about a leaky roof or a cracked slab. They will tell you it’s about a broader concept known as "agency".

Many new licensees treat "agency" as a vocabulary word they memorized to pass the state exam, but in reality, California real estate agency relationships are the legal foundation of your entire career.

Understanding how agency fits into the broader framework of California real estate laws—like the rules we cover in our California Real Estate Laws & Compliance Guide—is an important step in a long and prosperous career. If you get agency right, you can avoid the vast majority of problems.

If you don’t, you are walking through a minefield blindfolded.

What Is “Agency” in California Real Estate?

In plain English, agency is a legal relationship where one person (the principal) authorizes another person (the agent) to act on their behalf with third parties.

In California real estate, there are three key players:

The Principal: The client (buyer or seller).

The Agent: Technically, this is the Broker under whom your license hangs.

The Third Party: The person on the other side of the deal who you don’t technically represent.

Important Concept: There is a common misconception that you—the salesperson—are the "agent." Under California law, the Broker is the agent of the principal. You are an agent of the Broker. You act on the Broker's behalf to serve the client.

How an Agency Relationship Is Created

This might sound strange, but you don’t always need a signed contract to create an agency relationship. California law recognizes several ways to create this relationship:

1. Express Agency The "typical" and safest way to create agency. The principal and agent expressly agree to the relationship, usually via a written contract.

Crucial Update: Following the August 2024 NAR Settlement, "Express Agency" is no longer just a best practice for buyers—it is the rule. You are now required to have a signed Buyer Representation Agreement before touring a home. If you unlock a door without this contract, you are starting your career non-compliant.

Scenario: A seller signs a Residential Listing Agreement authorizing you to market their home, or a buyer signs a Representation Agreement before you show them a property.

2. Implied Agency Your actions lead a person to believe you represent them, even without a written contract.

Scenario: You represent the seller, but you start giving a potential buyer negotiation advice. Your conduct leads the buyer to reasonably believe you are advocating for them, creating an implied agency.

3. Ostensible (Apparent) Agency A principal allows a third party to believe someone is their agent, even if they aren’t formally authorized.

Scenario: A landlord knows you are showing their vacant units to tenants and doesn't stop you. Because the landlord allowed this, the tenants reasonably believe you have authority to act.

4. Agency by Ratification A principal accepts the benefits of an action performed by an unauthorized agent (or an agent acting outside their authority), effectively creating the agency retroactively.

Scenario: You present an offer to a "For Sale By Owner" seller who has not hired you. The seller likes the price, accepts the offer, and agrees to pay you. By accepting the benefit of your work, the seller "ratifies" the agency relationship for that transaction.

Crucial Note: Agency is about authority and behavior, not who pays you. You can owe fiduciary duties in real estate even if you’re not getting a commission.

Types of Agency You Must Know

Seller’s Agent (Listing Agent): You represent the seller exclusively. Your goal is to get the best terms for the seller while treating the buyer honestly.

Buyer’s Agent: You represent the buyer exclusively. This protects the buyer's interests in price and terms.

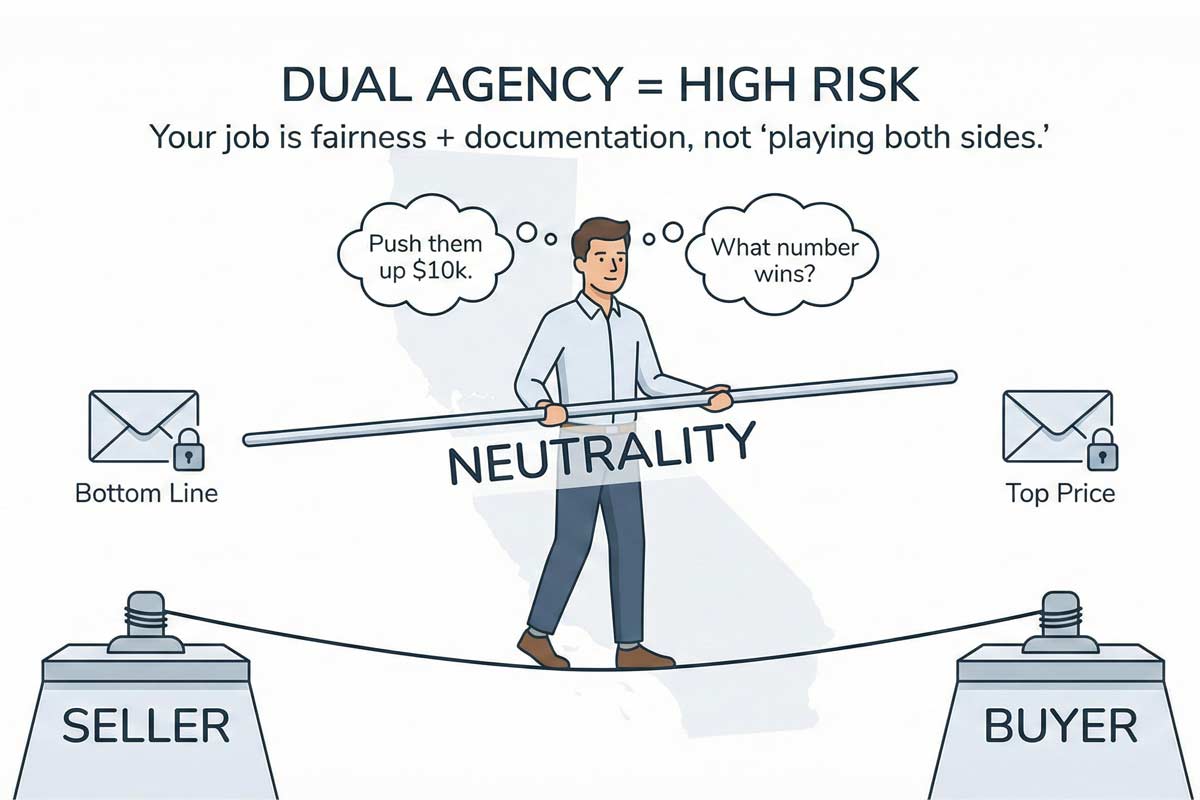

Dual Agency: The same broker represents both the buyer and the seller.

The Catch: In California, the Broker is the dual agent, meaning every salesperson under that broker falls under the dual agency umbrella for that transaction.

The Rule: You must remain neutral. You cannot tell the seller the buyer will pay more, nor tell the buyer the seller will take less, without express written permission. Undisclosed dual agency is one of the fastest ways to lose your commission and face a lawsuit. Courts and the DRE view undisclosed dual agency as a serious betrayal of trust.

Exam Tip: On the California real estate exam, agency questions often focus on how these relationships are created, what fiduciary duties you owe a client, and when dual agency must be disclosed. Expect questions that test whether you understand who the broker represents and what happens when you slip into undisclosed dual agency.

Fiduciary Duties: The “OLD CAR” Framework

Once you are an agent, you owe your client fiduciary duties—the highest duties known to law. I teach students the acronym OLD CAR to remember them:

O – Obedience: You must obey lawful instructions. If the client says “no open houses,” you don’t hold open houses.

L – Loyalty: You must put the client’s interest above your own. You cannot steer a client to a house just to get a higher commission.

D – Disclosure: You must disclose all material facts affecting the property’s value or desirability.

C – Confidentiality: You must keep your client’s price, terms, and motivation private forever.

A – Accounting: You must properly handle all money and documents entrusted to you.

R – Reasonable Care: You must act with the skill of a professional. If you don’t know the answer, don’t guess.

Agency Is the Hub of Compliance

Agency doesn’t exist in a vacuum. Your status as a fiduciary connects directly to every other major compliance area. Here is what agency looks like in the real world:

Disclosure (The “D” in OLD CAR)

Because you represent the client, you are the filter for information. You must strictly follow California disclosure laws to ensure every material fact reaches the client, protecting them from bad investments and you from negligence claims.

Trust Funds (The “A” in OLD CAR)

Your fiduciary duty of accounting means you must be meticulous with money. You must avoid commingling in California real estate, which involves mixing client trust funds with your own money—a major violation that triggers immediate DRE action.

Fair Housing (Duty of Care & Obedience)

Your duty of reasonable care requires you to understand California fair housing laws. You must treat all parties fairly and never inadvertently discriminate or steer clients, as this violates both federal law and your agency responsibilities.

Advertising (Honest Representation)

Even your marketing is tied to agency. The advertising laws for California real estate agents mandate that you clearly identify your license status and brokerage so the public is never confused about who you actually represent.

Required Agency Disclosure Forms (The DEC Process)

In most one-to-four unit residential transactions, you’ll follow the DEC process to ensure compliance:

Disclose: Provide the “Disclosure Regarding Real Estate Agency Relationship” (Form AD) before you sign a listing or write an offer.

Elect: Elect who you represent in your Listing Agreement or Buyer Representation Agreement.

Confirm: Confirm that same agency relationship again in the Purchase Agreement (RPA).

The Cost of Failure: This isn’t just paperwork. If you mishandle or fail to disclose agency properly, a court can decide you’re not entitled to a commission, even if you did all the work and closed the deal. A judge will not care how hard you worked if you were not legally authorized to perform the service.

Common Agency Mistakes to Avoid

In my years of consulting, I see the same agency mistakes repeated constantly. Here is what they look like in real life:

Accidental Dual Agency: You answer detailed strategy questions from a buyer at your open house and then write the offer without clearly disclosing dual agency. If the buyer later claims you were supposed to protect them, you’re now exposed as an undisclosed dual agent, which courts and the DRE treat very harshly.

Breach of Confidentiality: You tell a buyer’s agent, “My sellers are divorcing and need to sell fast,” without authorization. You’ve just handed the other side leverage and opened the door to a claim that you sabotaged your own client’s negotiating position.

Improper Trust Fund Handling: You accept an earnest money check made out to you personally instead of the title company or broker. Handling checks this way looks like commingling and can trigger an immediate trust account audit and potential license discipline.

How to Explain Agency to a Client (Script)

New agents often struggle to explain their role. Here is a simple script you can use to explain agency to a buyer or seller in 20 seconds:

“Mr./Ms. Client, I represent you in this transaction, which means I have a legal duty to put your financial interests ahead of my own. Everything you tell me stays confidential, and I’m required to disclose any facts that affect the value of the property so you can make the best decision possible.”

Using plain language like this builds trust immediately and sets the tone for a professional relationship.

Consequences of Violating Agency Law

The stakes are high. Violating agency law can lead to:

Civil litigation - Clients suing for damages if they overpaid or undersold because you mishandled agency.

DRE discipline - Suspension or revocation of your license.

Commission forfeiture - Courts can deny you a commission if your agency was not properly disclosed, even if you closed the deal.

Agency law is learnable. If you want to see how agency fits alongside disclosure, advertising, fair housing, and trust fund rules, spend time with our California Real Estate Laws & Compliance Guide so your entire business rests on solid ground.

|

The Fastest Way to Lose Your License

Imagine this scenario: You are a broker with a busy property management division. A tenant hands you a security deposit check for $2,000. You’re in a rush, so Read more...

The Fastest Way to Lose Your License

Imagine this scenario: You are a broker with a busy property management division. A tenant hands you a security deposit check for $2,000. You’re in a rush, so you deposit it into your general business operating account, intending to transfer it to the trust account on Monday.

Even if you transfer the money on Monday morning, you have already broken the law.

In California real estate, that mistake has a name: commingling of trust funds – illegally mixing a client’s money with your own.

Mishandling of trust funds is one of the most common reasons the California Department of Real Estate (DRE) disciplines licensees.

This article is part of our California Real Estate Laws & Compliance Guide, designed to keep you safe, compliant, and in business. Let’s break down exactly what commingling is, how it differs from conversion, and how you can avoid the audit nightmares that end careers.

What Is Commingling in California Real Estate?

In California real estate, commingling is the illegal practice of mixing a client’s money (trust funds) with the broker’s or agent’s personal or general business funds.

Think of it this way: As a real estate professional, you have two distinct "pockets."

Pocket A: Your money (commissions earned, operating funds).

Pocket B: The client’s money (earnest money, rents, security deposits).

Commingling happens when you put Pocket B money into Pocket A. Even if you don't spend it, the mere act of mixing the funds is a violation of the California Business and Professions Code.

Commingling vs. Conversion